What Happens If You Operate as an Unregistered MSB in Canada? (2026)

Regulators don't warn you twice. If your business moves money in Canada and you haven't registered with FINTRAC, you are already breaking the law. The Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) is explicit. Registration is the legal baseline for operating as a money services business in Canada. Here is what happens when you skip it.

Who Is an MSB in Canada?

Before we get to the penalties, you need to know if you're even an MSB.

You are one if your business does any of the following:

Foreign exchange: You exchange one currency for another.

Money transfers: You send, receive, or transmit funds on behalf of clients.

Money orders and traveller's cheques: You issue or redeem them.

Virtual currency: You exchange, transfer, or deal in crypto on behalf of others.

Payment services: You process or facilitate payments between parties.

If any of that describes your business, FINTRAC registration is a legal obligation under PCMLTFA s. 54(1).

The threshold is low. You do not need a storefront or high transaction volume. If the activity is regular and conducted for others, you qualify.

What the PCMLTFA Actually Says

Section 54(1) of the Proceeds of Crime (Money Laundering) and Terrorist Financing Act is direct:

Every person or entity that is a money services business shall register with the Centre.

"The Centre" is FINTRAC, the Financial Transactions and Reports Analysis Centre of Canada.

Registration requires you to submit your business details, beneficial ownership, and compliance program before you begin operating.

There is no grace period for accidental non-registration. You are either registered or you are in breach.

What FINTRAC Can Do to You

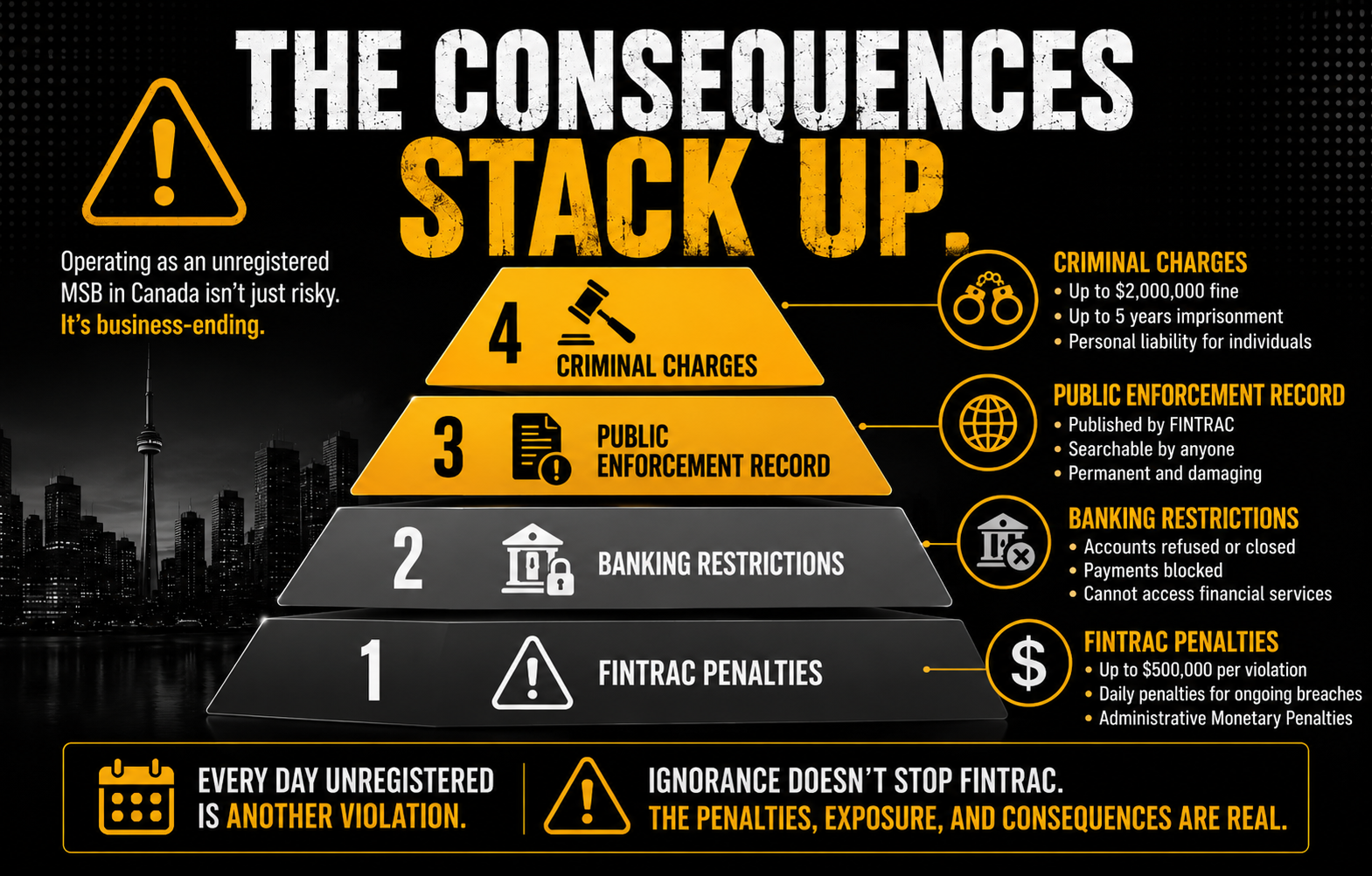

FINTRAC has two enforcement levers: administrative monetary penalties and criminal referral. They will use both.

Administrative Monetary Penalties (AMPs)

FINTRAC issues AMPs for violations of the PCMLTFA.

Penalties are categorized by severity: minor, serious, and very serious.

Failing to register is not a minor violation.

Very serious violations carry administrative penalties of up to $500,000 per violation for an entity. Every day of continued non-registration can be treated as a separate, ongoing violation.

FINTRAC publishes every AMP publicly with your business name, the penalty amount, and each violation listed. That record is indexed by search engines. It is permanent.

It affects your banking relationships, your investor due diligence reviews, and your future licensing in every jurisdiction you want to operate in.

Revocation of Registration

If you eventually register and then fall out of compliance, FINTRAC can revoke that registration. You have 30 days to appeal. After that, your ability to operate legally is gone.

Unregistered businesses face the same enforcement outcome, without ever having had the protection of a registration to lose.

The Criminal Exposure

Administrative penalties are painful. Criminal charges are business-ending.

Under sections 74(1) and 77.4 of the PCMLTFA, operating as an unregistered MSB can result in criminal prosecution. Section 74(1) covers general failures to register. Section 77.4 specifically targets anyone who knowingly conducts MSB activity without registration. Consequences depend on how the Crown elects to proceed.

On conviction by indictment: a fine of up to $2,000,000, imprisonment of up to 5 years, or both.

On summary conviction: a fine of up to $1,000,000 (or $250,000 for lower-tier offences), imprisonment of up to two years less a day, or both.

These penalties apply to the business. They also apply to individuals: directors, officers, and compliance officers who knowingly permitted the violation to continue.

If you are the compliance officer of a business operating without registration, you are personally exposed. Willful blindness is treated the same as knowledge under Canadian law.

The Business Consequences No One Talks About

FINTRAC penalties make headlines. The collateral damage is worse.

You cannot get a business bank account. Canadian financial institutions conduct AML due diligence on MSB clients. An unregistered MSB cannot pass that screening. Banks will refuse to open accounts or close existing ones once they discover your status.

You cannot onboard institutional clients. Any enterprise client in financial services will conduct vendor due diligence. An unregistered MSB fails that review immediately.

You trigger CRA scrutiny. Canada Revenue Agency shares intelligence with FINTRAC. An enforcement action from one regulator often invites examination from the other.

Your reputation does not recover quickly. FINTRAC's public penalty registry is searchable indefinitely. Your business name, the violations, and the penalty amount are all visible to anyone who looks.

Your investors are exposed. If you are a funded company operating without MSB registration, your investors may have material disclosure obligations. That creates downstream legal exposure across your cap table.

"But I Didn't Know I Was an MSB"

This comes up constantly.

The PCMLTFA does not require intent to prosecute. It requires a finding that you conducted MSB activity without registration. That finding alone is enough.

The definition of MSB activity has expanded significantly since 2014, and again with subsequent amendments. Virtual currency activities once considered grey-area are now explicitly covered. Payment service providers that previously operated without FINTRAC registration now fall squarely within scope.

If your business has grown since launch and you have not reviewed your regulatory status, there is a real chance your current activity triggers registration requirements you do not yet have.

Ignorance does not pause the penalty clock.

What to Do Right Now

If you are operating as an MSB without FINTRAC registration, the path is clear but it needs to happen immediately.

Step 1: Determine if registration is required. A qualified compliance professional can assess whether your activities trigger the PCMLTFA definition. Do not self-assess if you are unsure.

Step 2: Register before enforcement finds you. Voluntary registration before an enforcement action significantly changes your regulatory posture. FINTRAC distinguishes between businesses that self-correct and those that require compelled compliance.

Step 3: Build your AML program. Registration is not the finish line. You must have a documented AML compliance program in place, including a designated compliance officer, written policies, risk assessments, and staff training before registration is complete.

Step 4: Conduct a gap analysis. If you have been operating informally, assess your historical reporting obligations. There may be transactions that required suspicious transaction reports or large cash transaction reports that were never filed.

Unregistered exposure compounds over time.

The sooner you act, the smaller the remediation.

Get In Touch

Operating as an unregistered MSB in Canada is a federal offense with cascading consequences.

Administrative penalties up to $500,000 per violation for an entity. Criminal exposure of up to $2,000,000 and 5 years' imprisonment on indictment. A permanent public enforcement record. Loss of banking access. Investor liability.

FINTRAC's enforcement posture is not softening. It is getting sharper. The volume of enforcement actions is rising. Penalties are increasing. The scope of who qualifies as an MSB keeps growing.

You cannot outrun this by staying quiet.

Get ahead of it before FINTRAC does.

Book a Discovery Call to walk through your situation, understand what a two-week assessment involves, and determine which path applies to your operation.

These AMLI services are most directly relevant to operators in this position:

-

FINTRAC MSB Registration: Registration, renewals, updates, and regulatory correspondence management for MSBs at any stage, including operators managing an active deregistration or a change in business activity.

-

AML Audit and Effectiveness Review: A structured review of your AML program documentation, risk assessment, and evidence trail against current FINTRAC standards. Identifies gaps before an examiner does.

-

CAMLO and MLRO Services: Active compliance function ownership for reporting entities that need an embedded CAMLO without hiring one full-time. Covers day-to-day AML program management, regulatory coordination, and FINTRAC reporting.