Three Paths Forward for Canadian Crypto ATM Operators: Wind-Down, OTC Pivot, or Sale (2026)

If you operate crypto ATMs in Canada and the business is still running, you know it is no longer a question of whether the environment has changed. It has. Compliance obligations under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act have tightened. FINTRAC's enforcement posture has changed. Provincial regulators, particularly in British Columbia, have become more active. Banking relationships for ATM operators have become harder to maintain. And the unit economics of running compliant ATM infrastructure have deteriorated for most operators running between five and two hundred machines. This service exists because operators in this position need a structured way to assess their options and execute on one of them. A written plan, a cost execution, and a firm that has done each of these things before.

Why This Service Exists Now

The Canadian crypto ATM sector has operated under FINTRAC's MSB registration framework since virtual currency businesses became reporting entities under the PCMLTFA in 2014. For years, the compliance burden was manageable relative to the margins available. That calculus has shifted.

FINTRAC's administrative monetary penalties framework was overhauled in March 2026 under Bill C-12, raising maximum penalties by up to 40 times and introducing compliance orders as a formal enforcement tool. Operators running ATM fleets without robust AML programs, current risk assessments, and functioning transaction monitoring are now in a materially different risk position than they were 18 months ago.

At the same time, de-banking has accelerated. Several Canadian financial institutions have exited the crypto ATM space entirely. Operators who lose banking access mid-operation face an immediate compliance and liquidity problem that is difficult to resolve without outside support. In British Columbia, provincial regulatory pressure on ATM operators has added another layer of scrutiny that federal MSB registration alone does not resolve.

The commercial picture has also shifted. Higher compliance costs, lower transaction volumes on many machines, and reputational coverage associating ATMs with consumer fraud have compressed margins across the sector. Most operators who contact us have already done the math. They are looking for a structured way to address it.

AMLI built this service for that specific situation.

The Three Paths

Every engagement starts with a two-week assessment phase that produces a written recommendation and a cost execution plan. The recommendation identifies which of the three paths fits your operation. You review it, ask questions, and decide. If you proceed, AMLI executes. The assessment and the execution are separate engagements.

Here are the three options in detail.

Path One: Controlled Wind-Down

When this makes sense

If your crypto ATM operation is no longer commercially viable and you want to close it without creating regulatory or reputational exposure on the way out, a controlled wind-down is the appropriate path. This applies to operators who have already decided to exit the business and want to do it properly, operators whose banking relationships have collapsed and who cannot realistically rebuild them, and operators facing active FINTRAC scrutiny who need to close with a clean compliance record.

For a significant number of operators in the current environment, it is the most commercially rational decision. The question is whether it is executed properly or not.

What it involves in practice

A compliant wind-down under the PCMLTFA and FINTRAC's reporting obligations requires considerably more than turning off the machines. It involves ensuring all outstanding transaction reports are filed, handling customer balances and crypto inventory in a documented and compliant manner, formally deregistering the MSB with FINTRAC, satisfying any applicable provincial licensing requirements, and preserving records for the full retention period the legislation requires.

Done informally, a wind-down leaves the operator exposed to post-closure enforcement action. FINTRAC's examination authority does not end when the business stops operating. Done properly, through a structured process that closes each compliance obligation before the entity is deregistered, the file is closed cleanly.

What you keep and what you lose

You retain your compliance record, your ability to operate in regulated financial services in the future, and your personal and corporate reputation. You exit the ATM business. If the business has material value beyond the physical machines, that value may be recoverable through a sale rather than a wind-down, which is addressed in Path Three below.

Rough timeline

Four to twelve weeks, depending on the number of machines, the complexity of outstanding customer balances, and whether there are active FINTRAC correspondence items that require resolution before the deregistration is complete.

AMLI Analysis: The distinction between a regulated wind-down and an informal closure matters more than most operators expect. An operator who simply stops operating and lets their MSB registration lapse without filing outstanding reports or formally deregistering has not ended their FINTRAC obligations. Those obligations continue until the deregistration is confirmed. A wind-down managed as a compliance engagement closes each of those obligations in sequence, in the right order, with documentation.

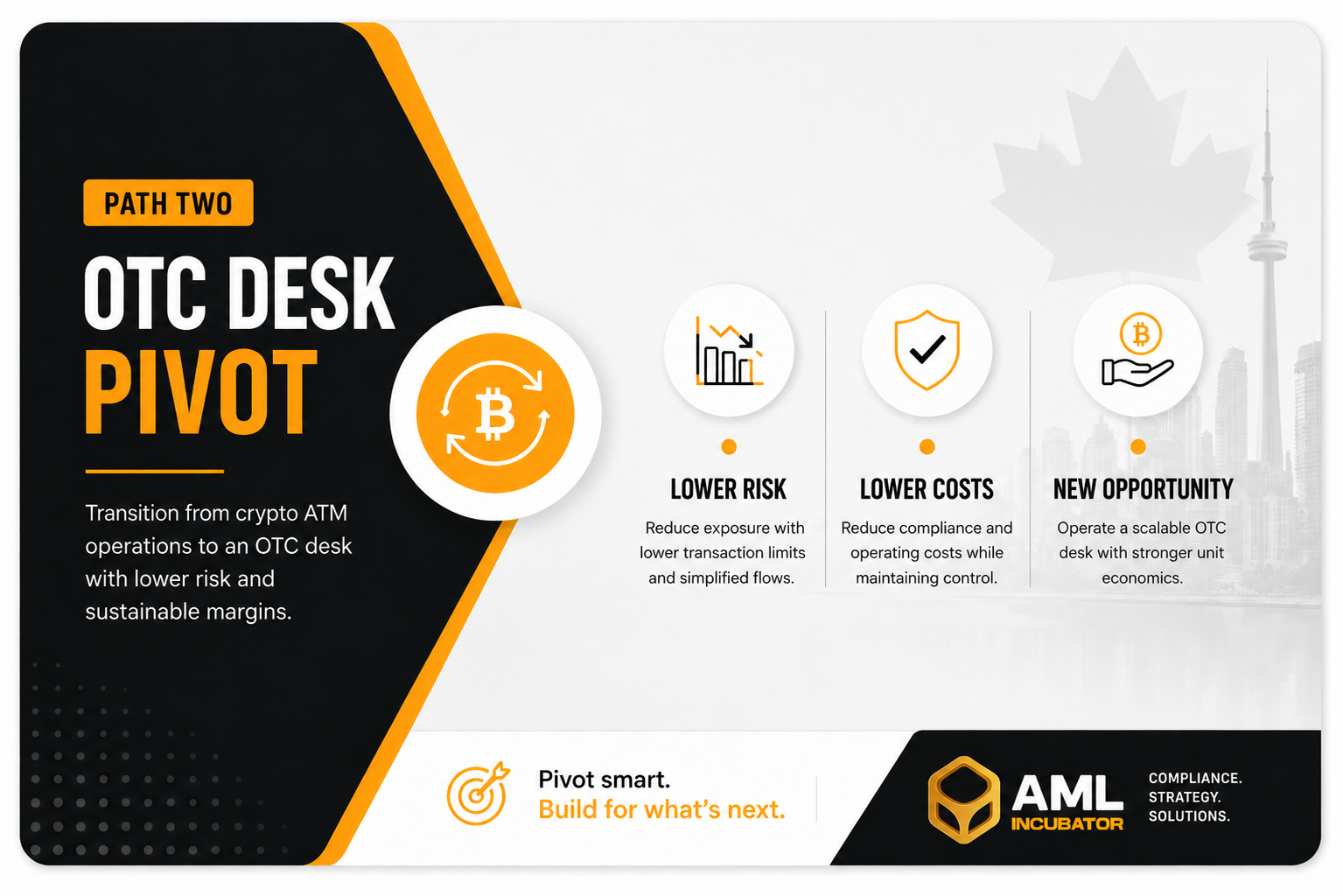

Path Two: Pivot to OTC Desk

When this makes sense

If your MSB registration, your AML program infrastructure, and your banking relationships are in good standing, there is a case for converting the business model rather than closing it. An Over-The-Counter virtual currency dealing operation serves a different client profile than an ATM network: fewer clients, larger transactions, stronger KYC requirements, and typically better unit economics per transaction. The infrastructure required to operate an OTC desk Canada-wide overlaps substantially with what a compliant MSB already has.

This path makes sense for operators who have the compliance infrastructure in place and a client base or market position that can support a pivot. It does not make sense for operators who need to solve a compliance deficit at the same time they are trying to build a new business model. Those two problems are not compatible in the same engagement.

What it involves in practice

The existing FINTRAC MSB registration covers virtual currency exchange and dealing, which is the core activity an OTC crypto desk Canada performs. The registration itself generally does not need to be re-obtained. What does need to change is the AML program, which must be rebuilt to reflect the OTC client profile and transaction structure. The risk assessment, the Know Your Client procedures, the ongoing monitoring framework, and the policies governing large-value dealing relationships all need to reflect the new operational model.

Banking relationships that have survived the ATM operation may be portable to OTC dealing, though this depends on the institution and the history of the relationship. Some institutions that have become uncomfortable with ATM operations will support OTC dealing under the right structure. Others will not. AMLI's active CAMLO outsourcing function can manage the regulatory side of this transition, including updated AML program documentation, revised risk assessments, and ongoing FINTRAC reporting under the new model.

What you keep and what you lose

You retain the MSB registration, the AML program infrastructure, and potentially the banking relationships. You exit the ATM revenue model and the physical machine infrastructure, which can be sold or wound down separately. The OTC operation is a different business. It requires a different client acquisition approach and a different compliance posture. Operators who treat the pivot as a minor operational adjustment rather than a business rebuild typically find it harder than those who go in with accurate expectations.

Rough timeline

Six to sixteen weeks for the full pivot, depending on how substantially the AML program needs to be rebuilt, whether banking relationships require renegotiation, and how quickly new OTC client relationships can be structured and onboarded.

AMLI Analysis: The OTC pivot is not the right path for every operator, and commercial honesty requires saying so directly. Operators who are already struggling with compliance deficits, who have had banking relationships terminated rather than voluntarily closed, or whose client base is primarily retail and anonymous are not well-positioned for an OTC desk. The OTC model requires a different kind of client: identified, vetted, transacting in larger volumes. The assessment phase exists specifically to determine whether the raw material for a viable OTC operation is actually present before recommending this path.

Path Three: Sell the Entity

When this makes sense

If your MSB registration is clean, your compliance record is in good standing, and you want to exit the business without operating it in any form, the regulated entity itself may have commercial value to a buyer. MSB registrations with clean FINTRAC records are not trivially obtained. The registration process takes time, the compliance history travels with the entity, and buyers who want a regulated virtual currency business in Canada will pay for one that does not come with compliance baggage attached.

This path is not available to every operator. If your registration has outstanding compliance issues, active enforcement items, or a history of examination findings, those will need to be resolved before a sale is viable. A buyer acquires the compliance record along with the registration. A record with unresolved issues reduces the value of the entity and can complicate or prevent the transaction.

What it involves in practice

AMLI has direct channels for MSB sale transactions. We can identify potential buyers for the entity, facilitate the connection, and manage the compliance-side documentation that a buyer's due diligence process requires. This includes a compliance record summary, current AML program documentation, FINTRAC correspondence history, and confirmation of current reporting status.

The sale of an MSB entity involves corporate and regulatory considerations that require legal counsel. AMLI is a compliance firm, and we work alongside legal advisors on these transactions rather than replacing them. Our role is the compliance execution and the buyer channel.

What you keep and what you lose

You receive proceeds from the sale and exit the regulated MSB relationship. What the buyer acquires is the registration and the compliance record, not necessarily the ATM fleet, which can be handled separately. The machines are assets; the MSB entity with its clean registration is a different asset. Both can be dealt with, and the proceeds from each are separate.

Rough timeline

Eight to twenty weeks, depending on buyer identification, due diligence timeline, and the complexity of the corporate structure being transferred.

AMLI Analysis: Operators often underestimate the value of a clean MSB registration in the current environment. The combination of a multi-year FINTRAC history with no outstanding enforcement items, a functioning AML program, and an active virtual currency dealing registration has genuine market value to buyers who want to enter the Canadian regulated crypto space without building that history from scratch. Whether that value is sufficient to make a sale preferable to a wind-down is one of the specific questions the assessment phase is designed to answer.

The Assessment Phase

Every engagement starts with a structured two-week assessment.

The assessment covers your current FINTRAC registration status and compliance record, your AML program documentation and any identified gaps, your banking relationships and their current status, your crypto inventory and customer balance position, your provincial licensing situation where applicable, and any outstanding FINTRAC correspondence that requires resolution.

The output is a written recommendation identifying which of the three paths is appropriate for your specific operation, with the reasoning behind the recommendation, and a cost execution plan for that path. You review the recommendation, ask questions, and decide whether to proceed. If you proceed, AMLI executes. If you decide not to proceed with any path, you have a written analysis of your situation that you can take to whichever firm or advisor you choose to work with.

The assessment fee is fixed and disclosed before engagement. It is separate from the execution engagement. These are two distinct decisions, and you make them separately.

AMLI Analysis: Operators sometimes ask whether they need the assessment if they have already decided which path they want. The answer is that the assessment is how we confirm whether the path you have identified is actually viable for your specific operation, and what it will cost to execute. An operator who has decided to sell, but whose compliance record has unresolved issues, needs to know that before committing to a sale engagement. The assessment protects both parties from engaging on a path that turns out not to be available.

Why AML Incubator?

AMLI provides outsourced Chief Anti-Money Laundering Officer services to reporting entities across Canada. Our practice covers FINTRAC and RPAA compliance, MSB registration and renewal, AML program design and effectiveness review, FINTRAC examination support, and CAMLO outsourcing for entities that need an active, embedded compliance function without hiring one full-time.

We have executed regulated MSB wind-downs.

Regulated wind-downs: structured, documented, with each compliance obligation closed in sequence and the deregistration completed cleanly. We have supported OTC desk conversions from ATM operator infrastructure, including AML program rebuilds and banking relationship reviews. We have brokered MSB sale transactions through our direct buyer channels.

They are things we have done for clients operating in the same environment you are operating in now.

We are not a law firm. We do not provide legal advice or legal defense services. For the legal components of any transaction or enforcement response, we work alongside legal counsel. The compliance execution is our role. The legal structuring is theirs.

Frequently Asked Questions

Will FINTRAC penalize me for shutting down?

A properly executed wind-down does not, on its own, trigger an administrative monetary penalty. Penalties arise from violations of the PCMLTFA and its regulations, not from the decision to exit the business. The risk in an informal or unplanned closure is that outstanding reporting obligations, record retention requirements, and the formal deregistration process are not completed. Those gaps can create post-closure exposure. A controlled wind-down managed as a compliance engagement is designed to close each of those obligations before the entity is deregistered, so that there is nothing outstanding when the file closes.

Can my existing MSB licence be used for an OTC business?

Yes, in most cases. FINTRAC's MSB registration covers virtual currency exchange and dealing, and an OTC desk performing those functions operates within the same registration category. The registration itself does not typically need to be re-obtained. The AML program, risk assessment, and KYC procedures do need to be updated to reflect the OTC operational model. Whether the registration requires any amendment to reflect the change in business activity depends on how your registration is currently structured and what specific changes are being made to the business.

What happens to customer balances and crypto inventory during a wind-down?

This is one of the more operationally complex elements of a wind-down, and it needs to be planned before the business closes rather than after. Customer balances that cannot be returned directly require a documented process with a clear paper trail. Crypto inventory needs to be liquidated or transferred in a compliant and documented manner. The specific approach depends on the structure of your operation and the nature of the balances involved. The assessment phase addresses this directly and produces a plan for handling it before execution begins.

How long does each path take?

Controlled wind-down: four to twelve weeks. Pivot to OTC desk: six to sixteen weeks. Sale of the entity: eight to twenty weeks. These are ranges based on typical engagements, not guarantees. The actual timeline for your operation depends on the number of machines, the state of your compliance documentation, the responsiveness of banking institutions, and in the case of a sale, the buyer's due diligence process. The cost execution plan produced after the assessment will include a timeline specific to your situation.

Will my banking relationships survive a pivot to OTC?

Some will. Some will not. The answer depends on which institution you bank with, the history of that relationship, and the institution's current appetite for virtual currency dealing businesses operating as OTC desks. This is one of the specific factors we assess during the two-week evaluation, and it is one of the variables that determines whether a pivot is viable for your specific operation. We do not guarantee that banking relationships will survive a pivot. Any firm that makes that guarantee is overpromising.

What does this cost?

The two-week assessment has a fixed fee that is disclosed in full before you engage. Execution fees vary by path and by the complexity of your operation. The cost execution plan produced at the end of the assessment gives you the full picture of what execution will cost before you commit to it. There are no open-ended retainers and no scope expansions without your explicit approval.

Can you help me sell rather than shut down?

Yes. If the assessment indicates that your entity has value to a buyer and your compliance record supports a sale, AMLI can manage the transaction process through our direct buyer channels. This includes buyer identification, compliance-side due diligence support, and documentation preparation. Legal structuring of the sale requires legal counsel. We coordinate with legal advisors and manage our side of the transaction, but we do not provide legal advice or replace legal counsel in the process.

Get In Touch

If your crypto ATM operation is at a decision point and you want a structured assessment of your options, the right starting point is a 30-minute call.

Book a Discovery Call to walk through your situation, understand what a two-week assessment involves, and determine whether one of the three paths applies to your operation.

These AMLI services are the ones most directly relevant to operators in this position:

-

CAMLO and MLRO Services Active compliance function ownership for reporting entities that need an embedded CAMLO without hiring one full-time. Covers day-to-day AML program management, regulatory coordination, and FINTRAC reporting.

-

AML Audit and Effectiveness Review A structured review of your AML program documentation, risk assessment, and evidence trail against current FINTRAC standards. Identifies gaps before an examiner does.

-

FINTRAC MSB Registration Registration, renewals, updates, and regulatory correspondence management for MSBs at any stage, including operators managing an active deregistration or a change in business activity.

Ready to get a clear picture of where you stand?

🌐 amlincubator.com

📧 hello@amlincubator.com