RPAA Registration Support Canada: What PSPs Need to Know (2026)

Payment firms rarely get stuck on strategy. They get stuck on execution. The pressure becomes visible when a product is live, counterparties are requesting proof of regulatory status, and internal teams begin to understand that RPAA registration support Canada is not a form-filling exercise. It is an operational readiness project that tests whether a business can accurately explain its model, document its controls, and support those claims when they come under scrutiny. For payment service providers entering or scaling in Canada, that matters in ways that show up quickly. A weak application can slow market entry, generate avoidable follow-up correspondence with regulators, and surface deeper gaps in governance, safeguarding, risk management, and compliance ownership. A strong application does more than move the registration process forward. It gives banks, partners, investors, and internal stakeholders the confidence that the business is being built on credible regulatory infrastructure, and that credibility creates commercial advantages that a rushed or poorly constructed application simply cannot provide.

What RPAA Registration Support Canada Really Involves

The Retail Payment Activities Act introduced a new regulatory framework for payment service providers operating in Canada and is administered by the Bank of Canada. For many firms, the practical challenge is not simply determining whether they are in scope. The real challenge is translating a functioning operating model into a regulator-ready submission that accurately reflects how money moves through the business, how risk is identified and controlled, and who holds accountability for each part of that picture.

That is precisely where support becomes valuable. Effective RPAA registration support Canada should cover significantly more than basic application administration. It should begin with scoping and entity analysis, then progress into control mapping, document development, gap assessment, and submission readiness. A provider whose service stops at helping a business complete fields in a portal is solving the smallest part of a much larger problem.

The more defensible approach is to treat registration as a cross-functional compliance workstream in which legal, operations, product, finance, information security, and compliance all contribute meaningful inputs. Someone within or supporting the business needs to consolidate those inputs into a coherent and consistent regulator-facing narrative. When that narrative breaks down under basic questioning, the root cause is rarely poor wording. It is almost always an underlying deficiency in governance design, process documentation, or control ownership.

Why Payment Firms Underestimate the Process

Founders and operators often approach RPAA registration with a degree of confidence built on the fact that they already manage payments, maintain internal procedures, and maintain active relationships with banking partners. That experience occasionally helps. It can also create significant blind spots.

An internal policy set constructed to satisfy commercial operational requirements is not automatically sufficient for regulatory review. The same applies to risk documentation developed for enterprise customer onboarding or board reporting cycles. The Bank of Canada and its supervisory staff are looking for something specific: clarity about accountability, evidence that the firm genuinely understands the risks generated by its payment activities, and demonstrable alignment between the narrative presented in the application and the way the business actually operates on a daily basis.

This is the point where applications most commonly stall. One team describes the business model in one way. Another team has documented it differently across internal policy. A third group operates an informal process that was never written down. None of those inconsistencies necessarily indicate that the business is noncompliant, but each one signals that the control environment is either immature or inconsistently documented, and both signals attract regulatory attention.

For fast-growth fintechs, this pattern is particularly common. Product evolves rapidly. Roles shift without corresponding updates to governance documents. Outsourced vendors assume a larger operational role than the original policies reflect. RPAA registration forces all of those accumulated realities into the open, often at a time when the business is under pressure from investors or commercial deadlines.

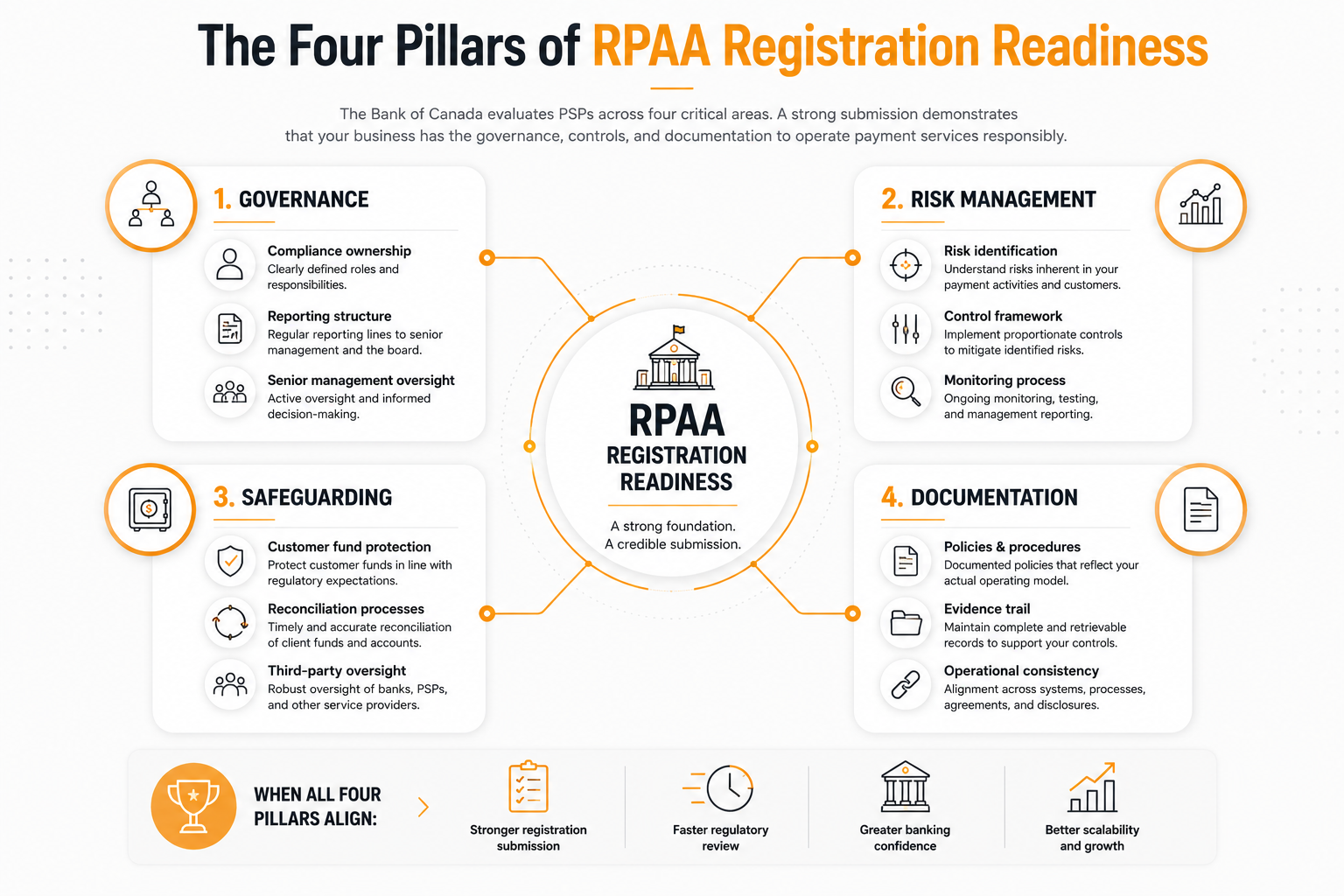

The Areas Regulators Will Focus on Most

A credible RPAA application typically stands or falls on a small number of core themes that run through every section of the submission.

The first is scope.

A business needs a legally defensible position on why the entity is in scope, which services it performs, where those services take place geographically, and which customer flows are captured by the framework. For businesses with layered corporate structures or international operations, this analysis becomes technically demanding very quickly.

The second is governance.

The regulator needs to understand who holds responsibility for compliance with the RPAA framework, how that responsibility is documented, how reporting flows to senior leadership, and whether senior management exercises genuine oversight rather than nominal sign-off. This does not require a large in-house compliance function, but it does require unambiguous ownership and documented decision-making authority at appropriate levels of the organization.

The third is risk management and safeguarding.

Payment businesses frequently have partial controls in place, but registration requires those controls to be described in a coherent and independently supportable way. If safeguarding arrangements depend substantially on third-party institutions, that dependency needs to be clearly understood, documented, and connected to the firm's own oversight responsibilities. If incident response currently sits within a broader technology function, the specific implications for payment activity still need to be addressed separately.

The fourth is operational consistency.

The application, internal policies, customer-facing terms, vendor arrangements, and actual workflows should not contradict each other. Reviewers will test this consistency by asking follow-up questions, and the weaknesses it reveals are usually not drafting problems. They are structural problems in the governance or process design that no amount of polished language can obscure.

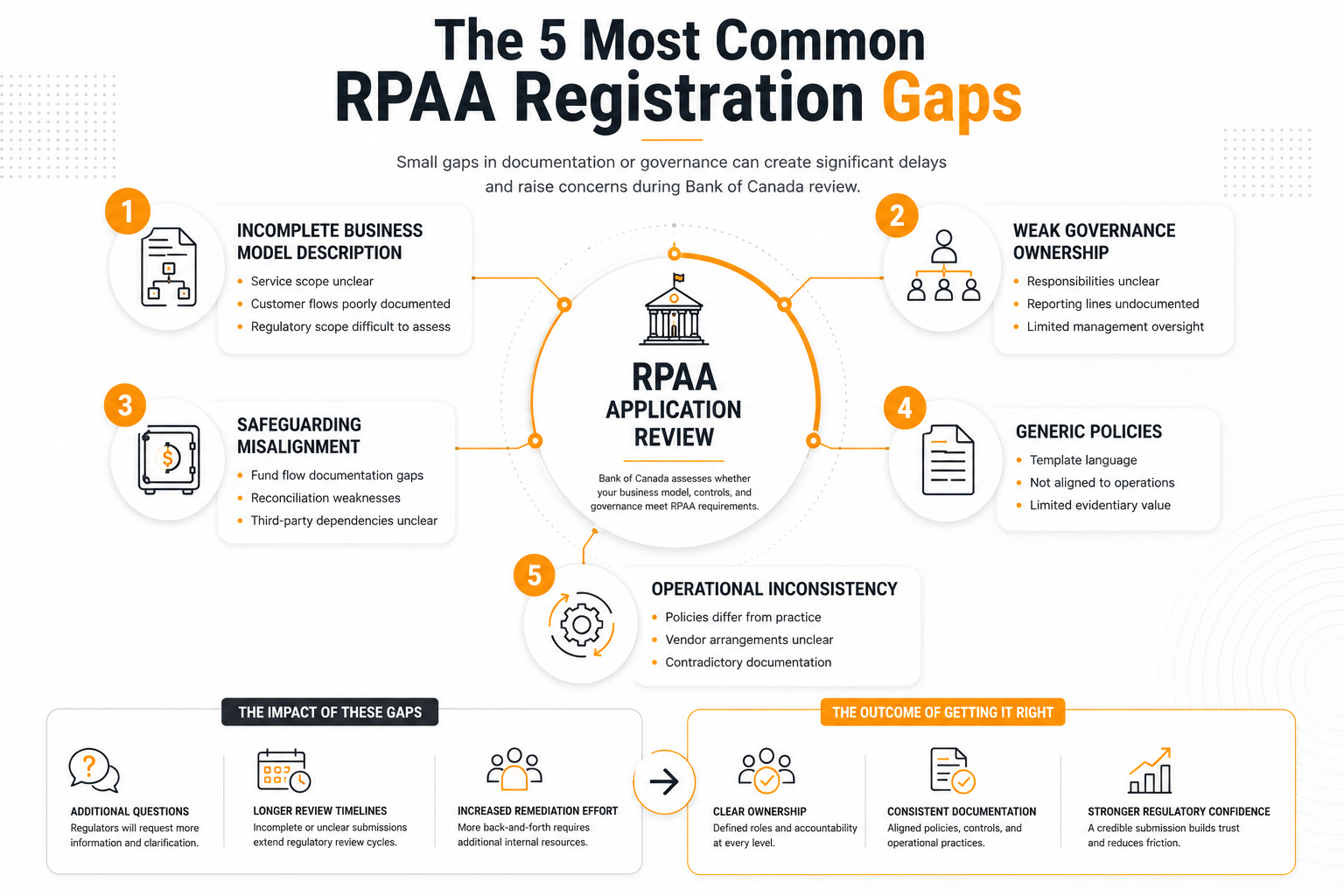

Where RPAA Applications Tend to Break Down

Most registration problems are not dramatic failures in a single section. They are cumulative. A business description is pitched at too high a level of abstraction. A control owner is identified by title but not by name or documented mandate. An outsourcing relationship is acknowledged but never fully explained in terms of risk allocation or oversight. A safeguarding narrative reads well on the surface but does not align with the actual account structure or reconciliation process when reviewers look more closely.

A second common failure point is overreliance on generic documentation. Templates and policy frameworks can help teams organize their thinking and structure initial drafts, but generic policies rarely survive meaningful regulatory review without substantial adaptation to the specific business model. Payment architectures differ. Wallet structures differ. Fund flows differ. Settlement timing differs. Regulatory reviewers who examine multiple PSP applications in a given period will notice when a submission contains standard language that does not match the specific operational detail described elsewhere in the same application.

Cross-border businesses encounter an additional layer of complexity. A firm operating across multiple jurisdictions with a single technology platform may need to demonstrate how the Canadian payment activity fits within that broader operating model without creating confusion around accountability, customer classification, or control coverage at the Canadian entity level. This requires careful scoping work before a single word of the application is drafted.

Timing introduces its own risk profile. When preparation begins too late, internal teams end up making foundational decisions under deadline pressure, decisions about which entity performs which function, how incidents are escalated, and how records are maintained that should have been resolved months earlier. RPAA registration support Canada delivers the most value when it begins before submission pressure makes careful thinking difficult.

What Good Support Looks Like in Practice

Good RPAA registration support reduces the internal burden on the business while improving the regulatory quality of the submission. That means someone external is actively driving the workstream, challenging assumptions about how the model is documented, and translating operational complexity into defensible regulatory language. It also means surfacing material issues early, well before those issues surface as regulator questions during the review process.

In practice, engagement typically begins with a structured diagnostic that covers business model scoping, a review of current-state documentation, identification of missing controls or unclear ownership, and development of a realistic path to submission readiness. From that foundation, the process moves into remediation and drafting. Policies may require substantive revision rather than light editing. Governance roles may need to be formally documented for the first time. Risk descriptions may need to be rebuilt to align with actual payment flows and the systems that support them.

The most effective advisors in this space do not approach RPAA work as a theoretical compliance exercise. They understand how payment service providers, fintechs, and embedded payment models actually operate, where the gap between product language and compliance language tends to widen, how banking expectations interact with regulatory expectations, and how to move a business toward a submission that will hold up without slowing commercial momentum more than necessary.

This is where specialist firms such as AML Incubator tend to generate meaningful value. The advantage is not only technical knowledge of the RPAA framework. It is the capacity to execute across documentation, governance, risk assessment, and operating model alignment within sectors where complexity and speed of change are both constants.

How to Prepare Before You Seek RPAA Registration Support Canada

Before engaging external support, gathering the materials that reveal how the business actually operates will accelerate the diagnostic phase substantially. That typically includes corporate structure documentation, product descriptions and user journeys, fund flow maps, outsourcing and vendor arrangements, safeguarding account details, incident management procedures, information security documentation, and any existing compliance materials. The purpose of this exercise is not to present everything in a polished state. It is to make gaps visible before a regulatory review makes them visible first.

Identifying an internal owner for the registration workstream is equally important. Projects that assign coordination responsibility to a single person who can connect legal, operations, finance, product, and compliance inputs consistently outperform projects where those functions operate without a clear point of integration. Even when most of the execution is handled externally, internal ownership still determines how quickly decisions get made and how consistently information flows across the project.

Businesses that are realistic about their compliance maturity at the outset make better decisions throughout the registration process. Some firms are close to ready and primarily need drafting support, technical review, and submission management. Others require deeper remediation before the application will credibly represent the business to a regulatory audience. Neither situation is unusual, and neither is a disqualifying condition for successful registration. What matters is knowing which situation applies before deadlines begin to drive decisions that should be driven by analysis.

Choosing the Right RPAA Registration Support Partner

Not every compliance provider is equipped for RPAA work. Some have strong generic policy drafting capabilities but limited depth on payment-specific operational requirements. Others understand registration mechanics but cannot assist with the governance and control framework that needs to sit behind the filing and support it under examination.

A strong RPAA registration support partner should be able to assess entity scope, identify regulatory and operational gaps, draft or significantly revise required materials, coordinate inputs across internal functions, and help the business respond clearly and consistently if questions arise from the regulator. They should also understand the adjacent pressures that PSPs navigate simultaneously, including AML obligations under the PCMLTFA, banking due diligence requirements, vendor dependency risks, and the accountability expectations that boards and investors increasingly apply to compliance infrastructure.

Those adjacent pressures are connected in practice even when they appear under separate regulatory headings, and RPAA work should not be siloed from them. A registration that reads well on paper but exposes weaknesses during a subsequent bank review, audit, or supervisory examination is only a partial success. The better outcome is a registration process that leaves the business more structured, more credible in its banking relationships, and better positioned to scale without rebuilding its compliance foundation at each stage of growth.

If your firm is preparing for RPAA registration, the objective is not to produce the longest application or the most polished language. It is to present a clear, supportable picture of how your payment business operates and how risk is identified and managed within it. When that foundation is solid, the registration process becomes significantly more manageable, and the business is better positioned for everything that comes after.

Get In Touch

Operating without completed RPAA registration is an unresolved regulatory exposure that affects banking relationships, commercial partnerships, and investor confidence simultaneously.

The Bank of Canada's supervisory program is active. The scope of who qualifies as a PSP under the RPAA continues to be interpreted broadly. The documentation and governance standards required for a credible submission are more demanding than most operators anticipate before they begin.

You cannot resolve this by deferring it.

Get ahead of it before it surfaces in a bank review, a partner due diligence process, or a supervisory inquiry.

Book a Discovery Call to walk through your situation, understand what a structured RPAA readiness assessment involves, and determine which path applies to your operation.

These AMLI services are most directly relevant to PSPs preparing for RPAA registration:

-

RPAA Registration Support: End-to-end registration support for payment service providers at any stage, including scoping, documentation, governance design, and submission management.

-

AML Audit and Effectiveness Review: A structured review of your compliance program documentation, risk assessment, and evidence trail against current regulatory standards. Identifies gaps before a regulator does.

-

CAMLO and MLRO Services: Active compliance function ownership for PSPs and reporting entities that need an embedded compliance officer without hiring one full-time. Covers day-to-day program management, regulatory coordination, and reporting obligations.