19.11.25

Written by Haik Kazarian, Head of business Development

Reviewed by Tigran Rostomyan, Compliance Expert

What Canadian MSBs Can and Cannot Do: A Complete Guide to FINTRAC Categories

Many businesses enter the Canadian fintech landscape assuming that Money Services Business status opens the door to every financial activity. In reality, FINTRAC classifies MSBs very specifically. Each category has a strict boundary, and crossing those boundaries can trigger consequences that reach far beyond the PCMLTFA. These include Bank Act restrictions, securities law exposure, retail payments regulation, and trust law issues.

This guide examines every MSB category in depth. It explains what you can realistically do, what you cannot do under any circumstance, and why these rules exist. It also explores grey areas and operational pitfalls.

If you operate in FX, remittances, payments, crypto, crowdfunding, cheque cashing or armoured car services, this is the definitive reference you can bookmark, share with partners and rely on during product design. This article also complements your other MSB-related reads, including What Qualifies as an MSB and Understanding MSB Licensing Requirements in Canada.

Understanding the Scope of Canadian MSBs

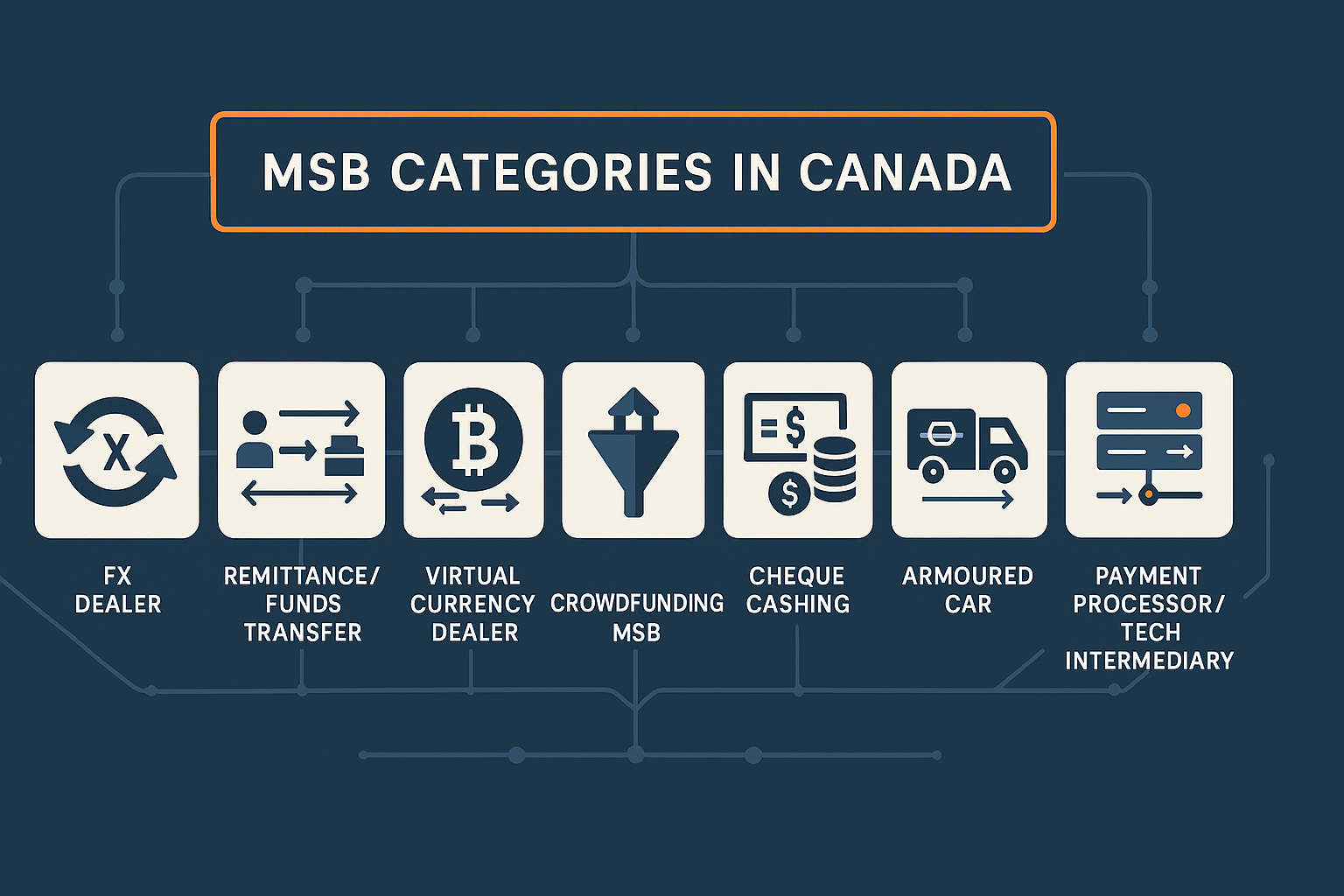

FINTRAC considers you an MSB if you are in the business of performing at least one of the following core services:

- Foreign exchange dealing

- Remitting or transmitting funds

- Issuing or redeeming money orders or similar instruments

- Dealing in virtual currency

- Operating a crowdfunding platform

- Cheque cashing services

- Armoured car services handling currency or negotiable instruments

Canada’s interpretation of MSB activity is stricter than many other countries. Payment services that merely touch client funds, even briefly, can qualify. Crypto platforms that only process a conversion on behalf of merchants qualify. Invoice processors qualifying as remitters is now common.

The sections that follow break down each category in depth.

Why FINTRAC Draws Such Strict Lines

The goal of the MSB framework is to prevent companies from gradually drifting into regulated banking, securities, deposit-taking, or trust activities without oversight. MSBs operate in one of the highest-risk sectors reviewed by FINTRAC. The regulator draws tight lines to:

- Prevent businesses from functioning like unlicensed banks

- Stop unregulated lending and investment activities

- Ensure cross-border transaction flows remain transparent

- Support sanctions enforcement

- Reduce ML and TF exposure caused by anonymous or fast-moving payment channels

These rules help keep the financial system safe and also help MSBs avoid accidentally getting involved in areas controlled by the Bank of Canada, securities commissions, OSFI, provincial regulators, and trust laws.

SECTION 1: CORE PRINCIPLES ACROSS ALL MSB CATEGORIES

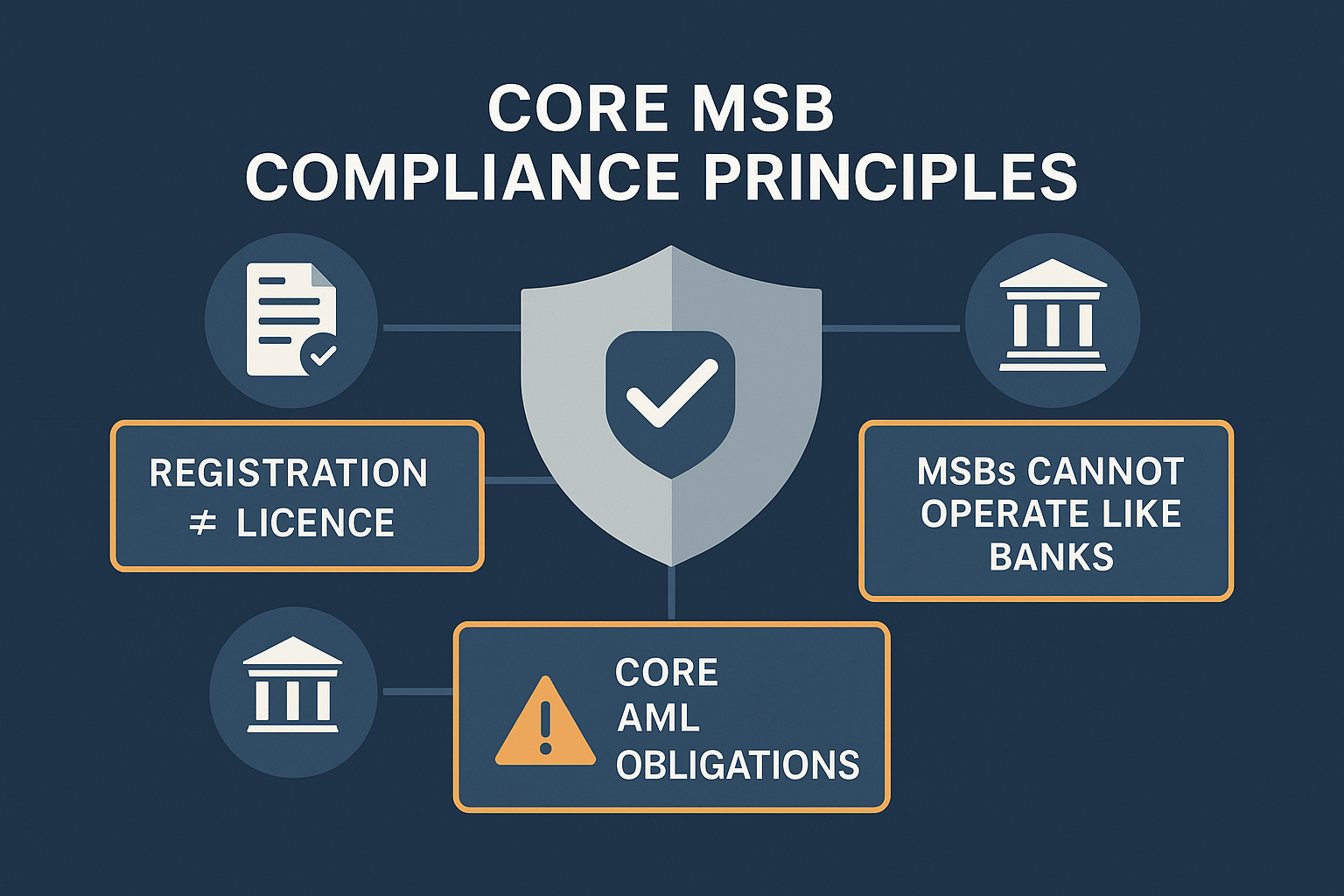

1.1 FINTRAC Registration Is Not a License

It is a registration, not an approval or endorsement. You cannot say your product is licensed, approved, certified, or authorized by FINTRAC. This applies to every MSB type.

Is FINTRAC registration the same as a financial license?

No. Registration only makes you a reporting entity under the PCMLTFA. Any functionality that resembles banking, securities, trust, or lending triggers other laws, not FINTRAC rules.

1.2 MSBs Cannot Operate Like Banks

Across all categories, the following activities are prohibited:

- Taking deposits

- Holding funds indefinitely without a clear payment purpose

- Offering interest

- Offering credit or overdraft

- Providing chequing features

- Issuing stored value functioning like a personal account

These functions fall under federal and provincial banking and lending rules.

1.3 Cross-Cutting AML Restrictions

Every MSB must avoid:

- Sanctioned persons

- Listed terrorist entities

- Transactions with no legitimate purpose

- Anonymous high-risk products

- Avoiding STRs, LCTRs and LVCTRs

- Ignoring ministerial directives

- Weak KYC practices

This will be repeated throughout the article, as these themes appear because most regulatory breaches come from ignoring these watchpoints.

SECTION 2: FOREIGN EXCHANGE DEALING (FX)

What FX Dealers Can Do

FX MSBs can operate in several ways:

• Exchange one fiat currency for another

• Offer spot FX trades at quoted rates

• Provide digital- or app-based exchange funded by bank transfer, wallet or card

• Apply spreads, commissions and service fees

• Provide 24- to 48-hour rate holds

• Combine FX with remittances

• Use third-party liquidity providers

• Act as principal or as agent

These operations are legitimate as long as the company does not resemble an investment dealer or a bank.

What FX Dealers Cannot Do

FX platforms must avoid activities such as:

• Offering investment-style products

• Providing forward contracts, swaps, derivatives or leveraged FX

• Giving FX investment advice

• Offering interest on stored balances

• Issuing credit

• Presenting themselves as licensed by FINTRAC

• Holding client money indefinitely without settlement

• Facilitating FX tied to sanctioned jurisdictions

FX dealers also must not ignore reporting obligations, which include suspicious transactions and cross-border reporting requirements.

Common Misunderstandings in FX

Many FX startups believe they can hold client funds for long periods for “later conversion.” In practice, this becomes a deposit-taking activity. FINTRAC treats long-term fund holding as evidence the business is doing more than FX.

FX dealers also underestimate sanctions risk. Cross-border USD transactions often face correspondent bank screening, and many FX MSBs lose banking relationships because they fail to screen for high-risk corridors.

Can an FX MSB provide hedging or forward contracts?

No. These activities fall under provincial securities and derivatives rules. An MSB cannot offer hedging products without additional licensing.

Scenario: FX Desk and the Line Between Trading and Securities

A Toronto based FX MSB offers CAD to USD conversions for SMEs. A client asks to lock in a USD rate for 30 days. The MSB agrees informally. This seems harmless, but the agreement is effectively a forward contract. Forward contracts fall under securities and derivatives regulation. Even if the MSB is well intentioned, this constitutes unregistered derivatives dealing.

SECTION 4: REMITTING OR TRANSMITTING FUNDS

This is one of the broadest categories. Many payment companies fall under it without realizing it.

What Remitters Can Do

- Send domestic and international money transfers

- Use SWIFT, EFT, wire, wallet or card networks

- Operate correspondent or agent models

- Process invoice payments where you receive money from the buyer and remit to the merchant

- Act as a payment gateway or merchant processor

- Combine payouts with FX

- Offer cash pickup, bank deposit, mobile wallet and card loads

These functions are fundamental to the Canadian payments landscape.

What Remitters Cannot Do

- Act as a bank account provider

- Offer unlimited stored value

- Hold client funds indefinitely

- Ignore RPAA obligations

- Provide credit or overdraft

- Facilitate transfers to sanctioned individuals

- Claim they are a bank or bank-like

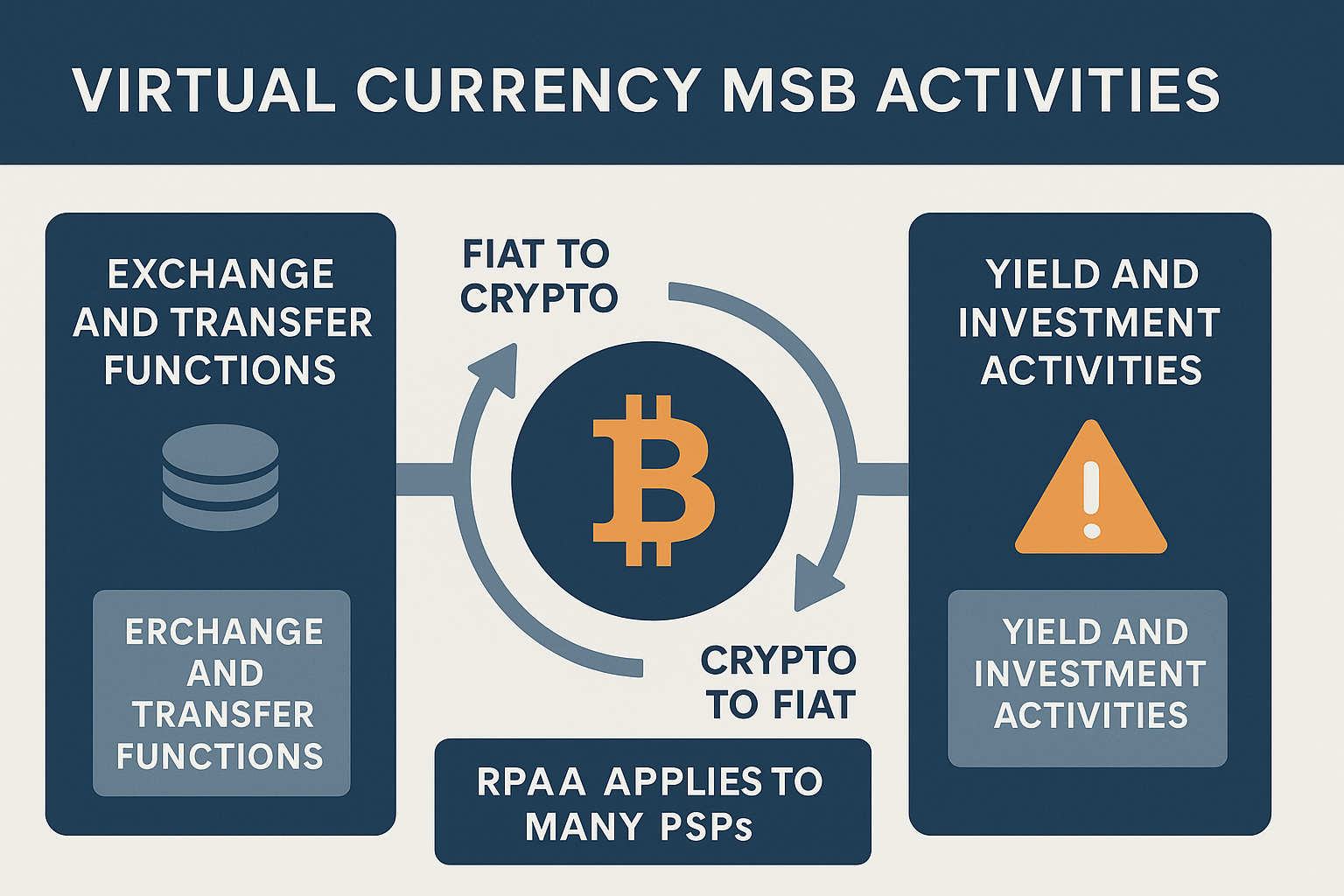

The Retail Payment Activities Act applies to many PSPs. When applicable, you must register with the Bank of Canada and comply with operational risk, safeguarding and incident reporting requirements.

Table: Remittance Activity Snapshot

Category | Can Do | Cannot Do

Remittance Services | Domestic and international transfers | Stored value accounts, credit, holding funds indefinitely

Common Misunderstandings in Remittance

Payment companies often assume that settlement delays from acquirers or banks are sufficient reason to hold funds for extended periods. FINTRAC evaluates the purpose of holding client funds. If the funds are not being held for immediate onward transmission, the MSB risks being categorized as deposit taking.

Another recurring issue is PSPs believing they fall outside MSB rules because they touch funds only indirectly. The moment a PSP receives money on behalf of a merchant, it is transmitting funds.

Does every payment processor automatically become an MSB in Canada?

Not always, but if a PSP receives funds from a payer and remits those funds to a payee, even through automated reconciliation, this is an MSB activity.

Scenario: Marketplace Payouts Trigger MSB Status

A Vancouver fintech runs a payment engine for online marketplaces. Buyers pay through their checkout system, and the fintech receives the funds into its pooled settlement account. After deducting marketplace fees, it forwards the remaining balance to merchants.

The founders assumed they were only providing software. During onboarding, their bank reviews the flow and points out that the fintech is receiving funds from one party and transmitting them to another, which meets FINTRAC’s definition of a remittance MSB. The one to three day settlement period confirms they are handling client funds, not simply passing data.

The bank requests an MSB registration number, an AML compliance program and proof the company is prepared for RPAA supervision. The founders realize their payment model falls squarely under MSB rules and must register before banking can proceed.

SECTION 5: DEALING IN VIRTUAL CURRENCY (VC)

Virtual currency MSBs operate in one of the highest scrutiny segments in Canada. FINTRAC applies a broad definition to ensure all entities handling crypto assets fall within the AML regime.

What VC MSBs Can Do

Virtual currency MSBs may:

- Operate crypto exchanges for fiat to crypto and crypto to crypto

- Run OTC desks

- Provide custodial wallets

- Process inbound and outbound crypto transfers

- Act as payment processors for crypto based checkouts

- Run crypto kiosks or ATMs

- Convert crypto to fiat for merchants

- Integrate crypto into e-commerce settlement flows

- Charge spreads, commissions and network fees

- Use multiple liquidity sources and custodial solutions

These activities are valid as long as the MSB remains within the conversion or transfer function.

What VC MSBs Cannot Do

VC MSBs cannot:

- Offer investment funds or pooled trading

- Provide yield, interest or staking as a service

- Give investment advice

- Ignore LVCTR reporting

- Offer anonymous mixers or tumblers

- Facilitate transfers associated with sanctions evasion

- Hold client assets indefinitely without purpose

- Provide leveraged crypto trading

- Market themselves as licensed by FINTRAC

Anything that resembles investment management or securitized crypto products immediately triggers CSA and CIRO oversight.

Common Misunderstandings in Virtual Currency

Crypto founders often assume that yield products are acceptable if the yield comes from staking or DeFi protocols. Canadian securities regulators treat most yield programs as unregistered securities. Even custodial wallet providers fall under investment rules if they allow clients to earn returns.

Another misunderstanding involves merchant crypto acceptance. If a platform accepts crypto on behalf of merchants and settles in fiat, it is generally considered both a VC dealer and a remitter.

Does running a crypto off-ramp make you an MSB?

Yes. If you receive VC from a client and remit fiat back, this is a virtual currency transfer service.

H4: Do all crypto ATMs require MSB registration?

Yes. Any kiosk that converts between fiat and VC is an MSB, regardless of whether it is self-operated or franchise-based.

Scenario: VC Merchant Gateway and the Dual Category Problem

A fintech offers a crypto checkout button for e-commerce merchants. Customers pay in crypto. The platform receives the crypto, converts it to CAD and remits CAD to the merchant. The founders believe they are only a technology layer. In practice, they are performing two MSB functions:

• VC dealing

• Remitting funds

The company now faces full MSB registration, LVCTR reporting, and travel rule compliance on top of merchant settlement obligations.

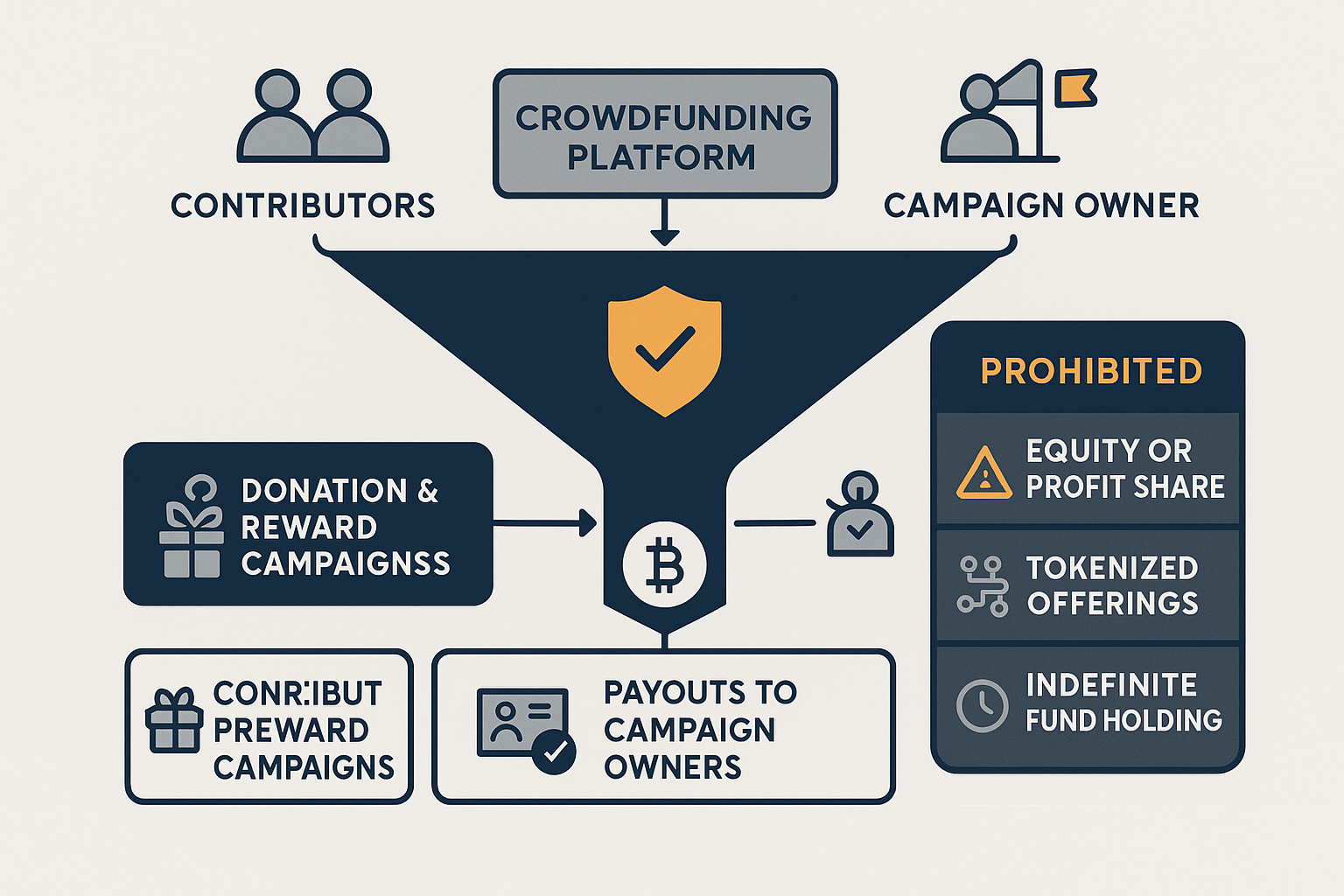

SECTION 6: CROWDFUNDING PLATFORM MSBs

Crowdfunding MSBs are relatively new in FINTRAC’s regime. The key distinction is that these platforms allow others to raise funds using the platform’s infrastructure.

What Crowdfunding MSBs Can Do

Crowdfunding MSBs may:

- Host donation-based or reward-based campaigns

- Support campaigns for charities, individuals or businesses

- Collect contributions in fiat or virtual currency

- Remit funds to the campaign owner

- Freeze or return funds due to fraud risks

- Conduct tiered KYC based on campaign type

- Charge platform fees and payout fees

- Manage disputes and cancellations

- Use payment processors as intermediaries

These activities are valid within the MSB framework as long as the platform does not cross into securities related fundraising.

What Crowdfunding MSBs Cannot Do

Crowdfunding MSBs cannot:

- Offer equity, bonds or profit-share instruments

- Offer token based fundraising that resembles securities offerings

- Hold contributions indefinitely

- Allow anonymous high-risk campaigns

- Run political fundraising without enhanced controls

- Facilitate fundraising for sanctioned entities or illegal purposes

Most prohibited activities fall under provincial securities rules.

Common Misunderstandings in Crowdfunding

Many platforms believe that “reward based” fundraising automatically avoids securities rules. In reality, if contributors receive anything that resembles future profits, revenue share or token value appreciation, the offering may fall under securities exemptions.

Platforms often underestimate beneficial ownership requirements. Campaign owners are not exempt from KYC. High risk campaign categories require deeper validation.

Does a platform become an MSB if it only holds funds temporarily?

Yes. The moment a platform receives funds and forwards them to a campaign owner, it becomes a remitter or crowdfunding MSB.

Can crowdfunding platforms support crypto-based campaigns?

Yes, but doing so classifies the platform as both a crowdfunding MSB and a virtual currency MSB.

Token-Based Crowdfunding Misclassified as Donations

A startup launches a platform intended for “reward-based fundraising.” Campaign owners offer early access tokens. Regulators identify that these tokens resemble investment contracts. The platform is now viewed not just as an MSB but as an unregistered securities marketplace. FINTRAC registration alone does not protect the company from CSA enforcement.

SECTION 7: CHECK CASHING SERVICES

Check cashers are MSBs because they exchange checks for cash. They often operate alongside remittance and FX services.

What Check/Cheque Cashers Can Do

• Cash payroll checks

• Cash government checks

• Cash other third-party checks

• Charge fees for check cashing

• Impose limits on unusual checks

• Combine check cashing with FX or remittances

• Perform enhanced verification for nonstandard checks

Check cashing services often operate in underserved communities and face elevated fraud risks.

What Cheque/Check Cashers Cannot Do

• Treat leftover funds as deposits

• Provide ongoing account features

• Ignore ID verification

• Cash checks drawn on sanctioned entities

• Avoid screening for stolen or fraudulent checks.

• Hold funds to create bank-like balances

• Provide credit secured by checks

Common Misunderstandings in Cheque Cashing

Cheque cashers sometimes believe that retaining a portion of cashed funds for future customer convenience is harmless. In reality, this resembles deposit taking. Even storing a balance of forty dollars until next week can be interpreted as account functionality.

Another issue is failing to screen for counterfeit or altered cheques. FINTRAC expects enhanced diligence due to fraud exposure.

Do cheque/check cashers need to verify every customer?

Yes. Identity verification and client risk assessment apply to all check cashing transactions.

Scenario: Unbanked Client Using Cheque Casher as a De Facto Bank

A client regularly cashes cheques and requests that the MSB hold the unused balance for next time. After several months, the MSB inadvertently acts as a bank account provider. This creates violations under the Bank Act and FINTRAC expectations.

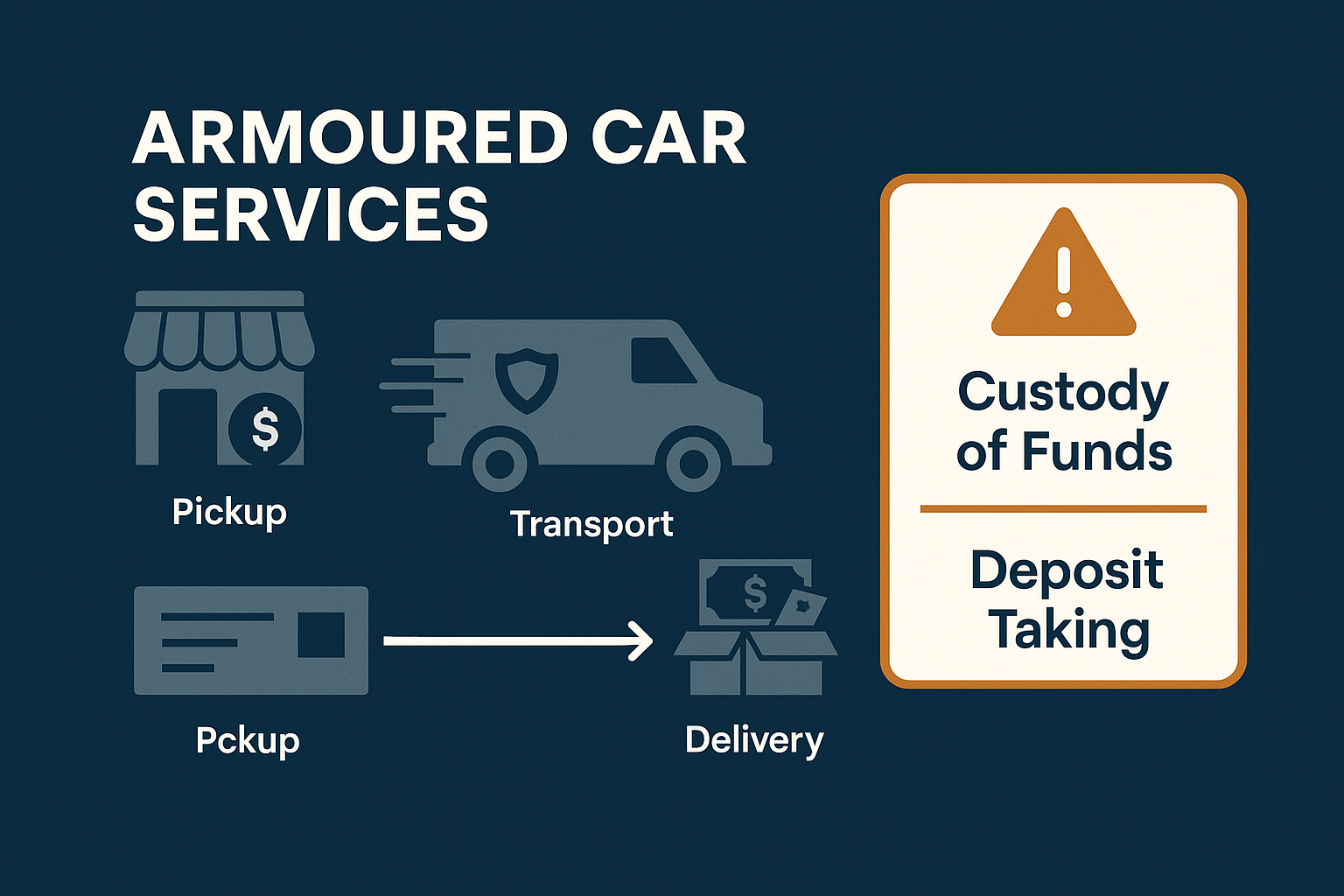

SECTION 8: ARMOURED CAR SERVICES

Armoured car services become MSBs when they transport currency or negotiable instruments.

What Armoured Car MSBs Can Do

- Transport cash between businesses and banks

- Move negotiable instruments

- Offer cash vaulting related to transport

- Secure retail cash pickups

- Deliver cash for ATM replenishment

- Support MSBs and casinos with cash handling

- Provide insured logistical services for currency movement

These activities fall squarely under the MSB category when tied to cash transport.

What Armoured Car MSBs Cannot Do

- Act like a deposit taking institution

- Hold funds overnight as operational balances unrelated to transport

- Ignore AML obligations if combined with FX or remittance

- Transport funds knowingly tied to criminal activity

- Provide account like storage

- Facilitate movement of funds to sanctioned entities

Common Misunderstandings in Armoured Car Services

Some operators assume that AML obligations do not apply if they are “just transporting.” If the service includes any form of custody or handling of funds beyond transport, FINTRAC expects MSB-level controls.

Armoured car services also sometimes underestimate how sanctions screening applies to the source and destination of funds.

Is a cash logistics company always an MSB?

Only when it transports currency or negotiable instruments as part of its commercial service. Pure logistics is not an MSB, but cash logistics is.

Scenario: Overnight Storage Interpreted as Deposit Taking

A cash transport company stores retailer cash in its vault for three days before delivering it to a bank. FINTRAC views this as custody rather than transport. If done regularly, it creates characteristics of deposit taking.

CROSS-CUTTING MISINTERPRETATIONS ACROSS ALL MSB TYPES

Across FX, remittance, crypto, crowdfunding, check-cashing, and armoured car models, certain misconceptions recur. These are the areas where both founders and international companies face delays, additional regulatory challenges, and strained banking relationships.

9.1 Holding Funds Too Long

Holding customer funds for reasons unrelated to immediate settlement or onward transmission is one of the clearest indicators of deposit taking. FINTRAC and banking partners view unexplained fund retention as a red flag. This applies across all MSB categories.

9.2 Assuming FINTRAC Registration Covers Every Financial Activity

MSB registration is frequently misunderstood as a license to operate like a bank or securities dealer. Any feature that resembles investment management, trust activity or product-based fundraising falls under other laws.

9.3 Believing Technology-Based Intermediaries Are Not MSBs

Payment processors, invoice platforms, and marketplace settlement providers often assume they are exempt because they operate as “technology companies.” The moment a company receives, holds, transfers, or converts funds on behalf of users, MSB rules apply.

9.4 Underestimating Sanctions Controls

Many MSBs incorrectly assume their banking partner is responsible for sanctions screening. FINTRAC expects MSBs to perform sanctions checks independently. This misunderstanding is one of the most common sources of compliance findings.

9.5 Overlooking Provincial Securities Legislation

In crypto, crowdfunding, and FX, the boundary with securities law is easy to cross. Yield, staking, futures, token presales, and forward contracts can trigger CSA enforcement even when the company has strong AML controls.

CONCLUSION

Canadian MSB categories are broader and more complex than many fintech founders expect. The lines between permitted and prohibited activities are sharp, and crossing them can create regulatory exposure across banking, securities, trust and payments law. Understanding the exact boundaries helps companies build compliant products, navigate bank onboarding and avoid unintended licensing problems.

This guide provides the full picture. Whether your business operates in FX, payments, VC, crowdfunding, cheque cashing or cash transport, the Canadian framework is clear once these rules are mapped properly. If a business plans to expand into Canada or scale its operations, knowing these boundaries early protects timelines, partnerships and regulatory relationships.

READ MORE HERE

• What Qualifies as an MSB

• Understanding MSB Licensing Requirements in Canada

• FINTRAC Banking Expectations for MSBs

• Why FINTRAC Is Delaying Your MSB Application

• Risk Based Approach

• Crypto MSB Essentials