FINTRAC MSB Revocation: What It Means, Whether It Can Be Reinstated

Most FINTRAC MSB revocations are not about wrongdoing. They are about process gaps, missed clarification requests, stale registration information, and compliance functions that could not produce evidence fast enough when it mattered. The good news: where the issue is administrative, revocation is not always the end of the road. AMLI has successfully reinstated revoked MSB registrations in Canada, and we can do the same for yours.

FINTRAC MSB revocation is serious. It means the business is no longer legally recognized as a registered MSB in Canada. It means banking relationships come under pressure. It means clients start asking questions. It means operations stop.

But we can get it reinstated.

Through a disciplined, evidence-based review process, AML Incubator has successfully supported MSBs through reinstatement back to active registration status with the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC). MSB reinstatement in Canada is possible, but it requires speed, the right expertise, and a compliance team that knows exactly how FINTRAC's review process works. We believe many businesses are sitting on similar risks right now, often without knowing it.

FINTRAC administers a registration framework that exists for good reasons, to protect Canada's financial system and maintain integrity in the money services sector. FINTRAC does exactly what it is required to do under the law. It is about understanding how revocations happen, what the recovery process looks like, and what it actually takes to come out the other side.

If your MSB registration is under pressure right now, or if you just want to make sure it never is, keep reading.

What FINTRAC MSB Revocation Actually Is (and Why It Is Not What Most People Think)

FINTRAC registration is not a licence. FINTRAC says so explicitly. It is a legal prerequisite for operating as an MSB in Canada, and it is a live regulatory status, not a one-time filing that is supposed to sit quietly in a drawer.

That distinction matters more than most businesses realize. Your registration is only valid as long as the information on file is accurate, your responses to FINTRAC are timely, and your compliance obligations are being met. The moment any of those conditions slips, the registration is at risk.

FINTRAC publishes five grounds on which a registration can be denied or revoked:

|

Revocation Ground |

What It Means in Practice |

|

The business is not eligible for registration |

The entity does not legally qualify as an MSB, or a key principal has a disqualifying history |

|

Failure to answer a clarification request within 30 days |

FINTRAC sent a formal information request and received no adequate response within the 30-day timeline |

|

Failure to respond in a timely manner to demands for information from FINTRAC |

FINTRAC requested information and the business did not respond with adequate speed or completeness |

|

Failure to notify FINTRAC of updates to operating information |

Changes to name, address, ownership, or services were not reported to FINTRAC within 30 days |

|

Failure to provide assistance to the Centre |

The business did not cooperate with FINTRAC's regulatory functions, including examinations |

Look at that list carefully. Most of those grounds are administrative and procedural. That matters for two reasons. First, it means revocation does not automatically mean wrongdoing. Second, and this is the part that should give every MSB pause, it means a business with genuinely strong anti-money laundering (AML) practices can still lose its registration through process gaps alone.

Strong intentions do not protect you. Strong processes do.

AMLI Analysis: Your compliance program is only as strong as what you can prove exists. If producing your full FINTRAC correspondence history would take days, that gap is worth closing before someone officially asks for it.

What Happens the Moment Your FINTRAC Registration Is Revoked

Most businesses do not discover a revocation proactively. They find out when something else breaks.

A bank partner runs a periodic check and flags the registry status. A client searches the FINTRAC MSB registry and finds the business listed, but its registration status is no longer ‘Registered’ (e.g., expired or revoked). An internal audit surfaces the gap. The discovery rarely comes with warning. It comes as a consequence of something else, at exactly the wrong time.

And the consequences are immediate. FINTRAC is explicit: businesses whose registrations are revoked, expired, ceased, or denied are not considered registered and cannot legally operate as MSBs in Canada. There is no grace period. There is no partial operating status while you work things out.

Here is what typically follows:

-

Banking relationships come under pressure. Financial institutions conduct ongoing due diligence on MSB clients. An inactive FINTRAC registration is a material flag. Expect urgent conversations.

-

Payment processing can stall. Networks and processors that require active FINTRAC registration as a service condition will identify the gap. Transaction flows can be suspended quickly.

-

Client relationships are at risk. Counterparties with their own compliance obligations may treat an unregistered MSB as an unacceptable exposure. Contracts come under review.

-

Internal pressure arrives fast. Boards, investors, and senior leadership want answers, not just about what happened, but about what the plan is and how long recovery will take.

The pressure is not theoretical. It is operational, financial, and reputational, simultaneously, and it starts on day one.

AMLI Analysis: Being embedded as CAMLO means we had the file, the history, and the context to move on day one. In a 30-day timeline, the time saved on orientation is the time spent on recovery.

The 30-Day FINTRAC Review Timeline That Determines Everything

Here is the single most important piece of information, and we are not exaggerating.

FINTRAC allows a business whose registration has been denied or revoked to request a review of that decision within 30 days.

Thirty days.

Miss it, and the review route closes entirely. At that point, reinstatement is off the table and the only path back to legal operating status is a full re-registration, which takes time, preparation, and a compliance foundation capable of supporting a clean application.

This is why the first response to a revocation must be an immediate answer to four questions:

-

Where are we in the 30-day timeline?

-

What documentation do we have?

-

Is a review viable?

-

What does the evidence file look like right now?

AMLI Analysis: The post-mortem is for after. The review prep is for now. Confirm the revocation date, count forward 30 days, and put that deadline somewhere everyone can see it.

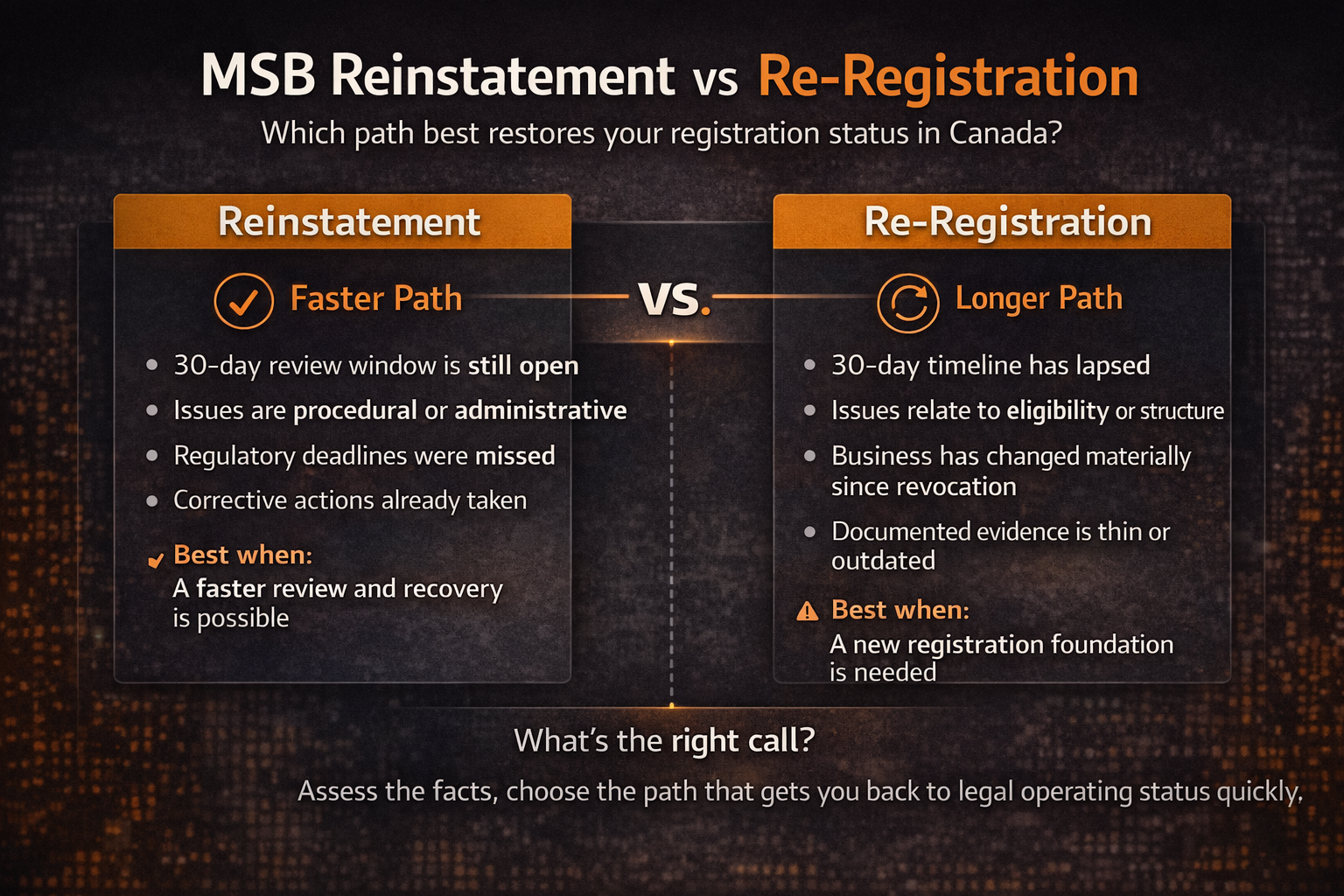

Two Roads: MSB Reinstatement in Canada vs Re-Registration

Once you know the revocation is real and the clock is running, you face a strategic call that will shape everything that follows. There are two possible paths, and choosing the wrong one can cost you weeks you cannot afford.

Road One: Review and Reinstatement

This is the faster path when the conditions support it. A review submission to FINTRAC, backed by organized evidence and clear corrective action, can result in reinstatement without going through the full re-registration cycle. This works best when:

-

The 30-day review timeline is still open

-

The revocation is rooted in a procedural or administrative issue rather than an eligibility problem

-

A credible, organized evidence file can be built quickly

-

Corrective actions have already been implemented and can be demonstrated

Road Two: Remediation and Re-Registration

Re-registration is not always the fallback option. Sometimes it is genuinely the right call. It may be faster and more defensible than a contested review when:

-

The 30-day timeline has closed

-

The business has changed materially since the original registration

-

The revocation touches eligibility rather than procedure

-

A fresh registration foundation serves the business better than defending the prior one

The goal is to get back to legal operating status as quickly and cleanly as possible. Sometimes that is reinstatement. Sometimes that is re-registration. A good compliance partner helps you make that call in the first 72 hours.

|

Decision Factor |

Pursue Review and Reinstatement |

Remediate and Re-Register |

|

30-day review timeline |

Still open |

Closed or nearly closed |

|

Nature of the issue |

Procedural or administrative |

Eligibility-based or structural |

|

Documentation quality |

Strong and can be assembled quickly |

Thin or does not reflect current reality |

|

Business changes since registration |

Business is materially similar to what was registered |

Significant operational or ownership changes have occurred |

|

Best when |

A clean evidence file can be built in time |

Re-registration is faster and more defensible |

AMLI Analysis: Fighting for reinstatement on principle when the evidence file cannot support it wastes the same time as re-registration, plus the 30 days you spent trying. Make the call on facts, not preference.

What a Successful FINTRAC Review of Revocation Filing Looks Like

A review submission to FINTRAC is not a letter of apology. It is not a narrative about good intentions. It is an evidence file, and it is judged on exactly that basis.

FINTRAC is assessing whether the specific revocation ground was incorrect, whether it has been remediated, or whether the business's actual operating position is different from what the record suggested. That assessment is based on what is in the file you submit. And not on what you intended or how strong your AML program is in theory on the file.

A strong review submission includes:

-

A factual, chronological account of what happened and when, without spin or deflection

-

A complete correspondence timeline: when FINTRAC communications were sent, when they were received, and what happened at each stage

-

Specific evidence that the revocation ground has been addressed, whether that is updated registration information, corrected documentation, or demonstrated response capability

-

A forward-looking remediation plan showing what structural changes have been made to prevent recurrence

-

Organized, indexed documentation, not a collection of files attached to an email

The submission should read as the work of a compliance function that knows exactly what happened, has fixed it, and can prove both. A disorganized or defensive submission will not improve the outcome regardless of how strong the underlying facts are.

AMLI Analysis: FINTRAC is not looking for resolution. Every document in the submission should answer one question: does this confirm the revocation ground no longer applies?

Why FINTRAC MSB Registration Revocation Is More Common Than Anyone Admits

FINTRAC reported 12 MSB revocations in its 2024-25 annual report. That number looks small. But it shows a pattern, and the pattern almost always traces back to the same structural gaps appearing across different businesses:

-

Registration treated as a one-time filing rather than a live document that requires active maintenance

-

FINTRAC correspondence routed through informal or unmonitored channels with no named owner

-

No escalation protocol for time-sensitive regulatory communications

-

Legal entity changes, restructuring, new ownership, new services, not connected to registration update obligations

-

No tested process for responding to formal FINTRAC demands quickly and completely

These gaps can exist quietly in a business for years. The registration stays active. Nothing breaks. Audits pass. And then a FINTRAC clarification request arrives, or a periodic review is triggered, and the invisible gap becomes visible at exactly the worst moment.

The businesses that avoid revocation are not necessarily more compliant in intent than the ones that face it. They have built administrative infrastructure that matches the regulatory seriousness of what they do. That is the difference.

Here is a practical test:

Could your current compliance setup catch and respond to a FINTRAC clarification request within 30 days, reliably, every time, regardless of who is in the office that week?

AMLI Analysis: Assign a single named person, not a team, as owner of FINTRAC registration maintenance. That person flags any operational or structural changes within 30 days. No assumptions that someone else has it covered.

Why an Outsourced CAMLO Changes the Outcome of an MSB Revocation

We want to be honest about something. A strong compliance function does not guarantee that no issues ever arise. Regulatory frameworks are complex, businesses evolve, and FINTRAC's processes involve timelines that can catch even well-run organizations off guard.

What a strong compliance function changes is whether the issue becomes terminal.

FINTRAC requires all reporting entities to maintain a full compliance program, whether that is run in-house or through an outsourced CAMLO.

The components are not optional:

-

A designated compliance officer with genuine authority and accountability

-

Written policies and procedures that reflect actual operations, not aspirational ones

-

A current, documented risk assessment

-

A training program with evidence of completion

-

Regular effectiveness reviews that test whether the program is working

FINTRAC also states clearly that delegating compliance duties does not remove the reporting entity's ultimate responsibility for implementation. You can share the work. You cannot share the accountability.

In a revocation scenario, a capable compliance function changes the trajectory in ways that matter:

-

It identifies a potential trigger before the 30-day timeline becomes critical

-

It preserves and organizes the communication trail from the moment an issue is flagged

-

It distinguishes between a procedural issue and an eligibility issue, which determines the recovery path

-

It builds a regulator-facing file that is organized, credible, and specific

-

It coordinates corrective action across legal, operations, and finance without losing time to the clock

The compliance function that looks like overhead during normal operations looks like survival infrastructure when a revocation lands. The question is whether you want to find that out before or after the crisis arrives.

AMLI Analysis: Ask your compliance provider: what would you do in the first 24 hours if we received a FINTRAC revocation notice today?

If Your FINTRAC Registration Is Revoked: What to Do in the First 72 Hours

If your FINTRAC registration has been revoked, denied, or is at immediate risk, the first 72 hours are disproportionately important. Here is the sequence that matters:

-

Confirm the exact registry status. Check the FINTRAC MSB registry directly. Revoked, expired, ceased, and denied each carry different implications and different recovery paths. Do not assume you know which one applies.

-

Establish where you stand in the 30-day review timeline. This is the governing deadline. If it is still open, everything else is organized around protecting it.

-

Preserve all FINTRAC correspondence without alteration. Do not archive, reorganize, or delete anything. Preserve the full record including metadata and timestamps.

-

Identify the precise revocation ground. Clarification request? Information demand? Registry update failure? Eligibility issue? The answer determines your entire strategy.

-

Reconcile the registration file against how the business actually operates today. Document every gap between the two.

-

Designate a single named owner for all FINTRAC communications, effective immediately.

-

Make the reinstatement versus re-registration call within 72 hours, with experienced compliance counsel. Not after extended deliberation.

-

Do not communicate with FINTRAC speculatively before you have an organized, accurate position. Everything you submit becomes part of the record.

We know this sequence because we have worked through it. The businesses that follow it in the first three days are in a materially better position than those that spend those days in internal debate.

AMLI Analysis: Responsiveness to FINTRAC matters. Accuracy matters more. Build the organized file first, communicate second. An uncoordinated early message can complicate the review process significantly.

FINTRAC MSB Revocation: Questions We Get Asked a Lot

Does a FINTRAC revocation mean my business committed a financial crime?

No. FINTRAC's published revocation grounds are primarily administrative and procedural, covering unanswered clarification requests, registry update failures, and untimely responses. The majority of revocations have no connection to money laundering allegations or criminal conduct whatsoever.

Is FINTRAC registration the same as a licence?

No, and FINTRAC makes this explicit. Registration is a legal requirement for operating as an MSB in Canada. It is not an endorsement, not a certification of compliance, and not a licence. It must be actively maintained to remain valid.

Can a revoked MSB request a review?

Yes. FINTRAC allows businesses to request a review of a denial or revocation within 30 days of the decision. That timeline is firm, and engaging experienced compliance counsel to assess your position quickly is essential.

What if reinstatement is not realistic?

Then the focus shifts to structured remediation and re-registration. AMLI has guided businesses through rapid re-registration that returned them to legal operating status efficiently and cost-effectively. Re-registration is not a failure. In some situations, it is the faster and cleaner path, and we will tell you honestly when that is the case.

Can we keep operating while pursuing reinstatement?

No. FINTRAC is explicit that businesses with revoked registrations are not considered registered and cannot legally operate as MSBs. There is no partial operating status during a review period. Operating without registration carries serious regulatory and legal risk for the business and its principals personally.

What does AML Incubator actually do in a revocation situation?

We assess the file and the clock immediately. We identify the precise revocation ground. We determine which recovery path is viable and advise directly. We build the evidence file for review or re-registration. We coordinate the corrective actions required and manage the FINTRAC-facing process from start to reinstatement or re-registration. We have done it. We can do it for you.

Get In Touch Now

If your FINTRAC MSB registration is under pressure, or if you want to reduce the risk of revocation before it becomes a live issue, these AMLI resources cover the operational areas that matter most.

CAMLO & MLRO Services for AML Compliance

Support for businesses that need ongoing compliance ownership, regulatory coordination, and stronger day-to-day control over AML obligations.

AML Audit & Effectiveness Review Services

A practical review of whether your AML program, documentation, and evidence trail are strong enough to stand up to regulatory scrutiny.

FINTRAC MSB Registration

Help with registration, updates, remediation, and regulatory response so your MSB status reflects how the business actually operates.

Ready to assess your position?

Book a Discovery Call to review your registration risk, identify administrative or compliance gaps, and assess whether reinstatement, remediation, or re-registration is the right path.