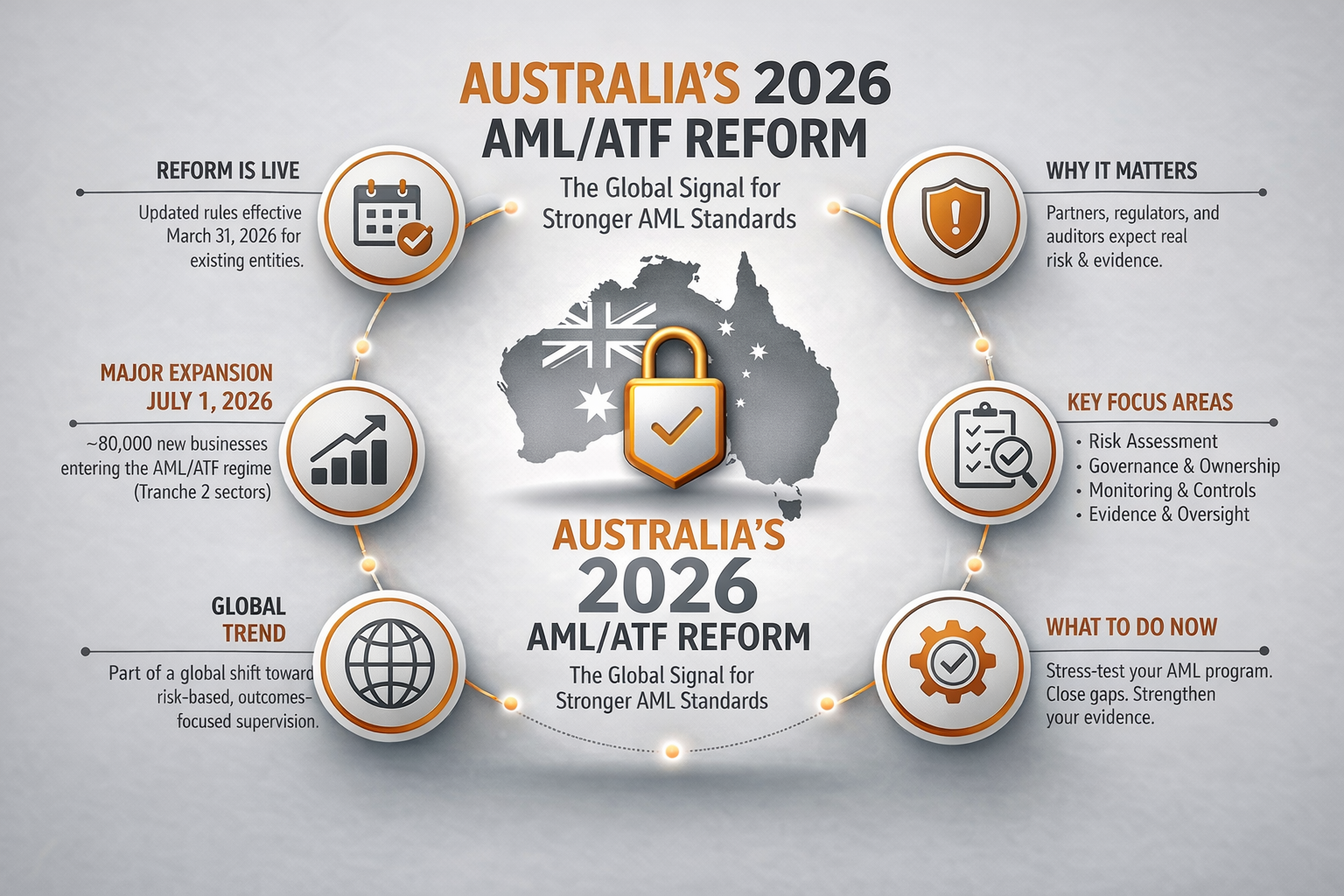

Australia’s AML Reform Is Live. Here’s Why Global Fintechs Should Pay Attention.

Australia’s AML/CTF reform is now live for existing reporting entities, and a much wider expansion arrives on July 1, 2026. For fintechs, money services businesses, and virtual asset service providers, the signal is larger than one jurisdiction. Regulators are moving toward more risk-based, implementation-focused supervision that tests whether controls match real exposure and whether firms can evidence how they manage financial crime risk. The businesses that adjust early will be in a stronger position for partner reviews, licensing discussions, and supervisory scrutiny.

Most compliance updates arrive quietly. They sit in a newsletter, get filed, and change nothing for six months. This one is different.

The AML reform of 2026 that will take effect in Australia on March 31 is not just a jurisdictional milestone. It is a leading indicator of where AML supervision is heading globally and what fintechs, MSBs, and VASPs everywhere should expect partners, auditors, and regulators to ask them next.

On March 31, 2026, updated AML/CTF obligations took effect for existing reporting entities in Australia. The next milestone lands on July 1, 2026, when newly regulated tranche 2 sectors will begin coming into scope. Australian Transaction Reports and Analysis Centre, AUSTRAC says the AML/CTF Australia reforms will extend the regime to around 80,000 additional businesses, including businesses in real estate, legal, accounting, and precious metals and stones.

For many fintech founders outside Australia, that may sound local. It is more useful to treat it as a regulatory signal.

Australia’s reform is part of a broader shift in AML supervision. The direction is toward a more risk-based, implementation-focused model that asks whether firms actually understand their exposure, whether controls are aligned to that exposure, and whether decisions can be evidenced. AUSTRAC has said the reforms place the importance of risk at the heart of its AML approach and that its regulatory focus is evolving toward reducing the harm caused by money laundering, terrorism financing, proliferation financing, and other serious financial crime.

Many firms first feel AML pressure through operations, long before a regulator is involved.

That matters to global fintechs because many firms first feel AML pressure through operations. A bank partner asks for your risk assessment. A processor wants to understand your transaction monitoring approach. A licensing or diligence process moves beyond policy documents and into governance ownership, control design, and recordkeeping. Australia’s AML reform matters because it makes those expectations more visible and harder to defer.

What changed in Australia’s AML/CTF framework

The AML/CTF Australia reform changes both scope and supervisory posture. Both matter, and they are somewhat interlinked.

At legal level, Australia has modernized its AML/CTF framework and expanded who is regulated. AUSTRAC says the new laws simplify and modernize the regime and align it with international standards set by the Financial Action Task Force. Existing reporting entities will move to updated obligations on March 31, 2026. Newly regulated sectors will begin entering the AML/CTF Australia regime from July 1, 2026.

At practical level, the reform pushes firms toward a more disciplined operating model. AUSTRAC’s reform materials repeatedly point businesses toward risk assessments, AML/CTF programs, governance responsibilities, staff readiness, recordkeeping, and implementation planning.

For current reporting entities that cannot meet all new or changed obligations by March 31, 2026, AUSTRAC says they should have a documented implementation plan explaining how risks will be managed during transition, how gaps will be addressed, and how required changes will be delivered. That is a useful detail because it shows the standard regulators increasingly care about. Not perfect paperwork on day one, but controlled implementation with visible ownership and risk management.

AMLI Analysis: This area is where many firms misread reform. They focus on commencement dates and miss the operating standard underneath them. The harder question is not "What date applies to us?” It says, “can we show how we are implementing, governing, and evidencing the changes?”

Why AML reform 2026 is a global signal, not an Australian one

Australia is not the only jurisdiction moving this way. The deeper relevance of the 2026 AML reform comes from the FCTF framework underneath modern AML regulation. FCTF describes the risk-based approach as the cornerstone of its standards, requiring firms and authorities to identify, assess, and understand risk so measures can be proportionate and resources can be directed where exposure is greatest.

That means the Australian reform should be read as part of a larger global pattern. Even where rules differ by jurisdiction, the underlying supervisory questions increasingly sound the same:

-

What are the firm’s actual ML/TF risks?

-

How do controls map to those risks?

-

Who owns those controls?

-

How often are they reviewed?

-

What evidence exists that the program is being maintained?

This is why non-Australian fintechs, MSBs, and VASPs should pay attention. They may not be subject to AUSTRAC directly, but they are increasingly being judged against similar operational expectations by partners, auditors, and regulators in their own markets.

How Australia’s reform compares to other major AML regimes

Understanding the AML reform 2026 in Australia is more useful when you can place it against what is happening in the jurisdictions your business already operates in or plans to enter. The direction is consistent. The pace varies.

|

Jurisdiction |

Direction of travel in 2025–2026 |

|

Australia (AUSTRAC) |

Outcome-based reform, live. Tranche 2 expansion: July 2026. 80,000 new entities entering scope. |

|

European Union (AMLA) |

New AML authority is operational. Direct supervision of high-risk obligated entities. Harmonized rulebook replaces fragmented national regimes. |

|

United Kingdom (FCA / NCA) |

Outcomes-focused supervision strengthened. SAR quality under scrutiny. Enhanced expectations for crypto and payments firms. |

|

United States (FinCEN / BSA) |

The AML Act of 2020 is being implemented. Beneficial ownership registry is live. MSB expectations are tightening around monitoring evidence. |

|

Canada (FINTRAC) |

Reviews of compliance program effectiveness are increasing. Named accountability for compliance officers was reinforced. |

The common thread is not the specific rule. It is the supervisory question underneath it: does the program actually work? For more on how these regimes interact with fintech-specific obligations, AMLI’s KYC vs AML explainer covers how the components of a full AML program fit together.

AMLI Analysis: A firm that builds its program to the Australian 2026 standard will be better positioned across all five of these jurisdictions, not just AUSTRAC. The supervisory questions are converging even where the rulebooks still differ.

What this means for fintechs, MSBs, and VASPs in practice

For operators, the AML reform 2026 matters less as a headline and more as a workflow issue. It raises the bar across four specific areas that together define whether a program is defensible.

Risk assessment quality

If your business touches payments, stored value, crypto conversion, cross-border flows, custody, or cash-out, your risk assessment needs to describe those exposures in operational terms. It needs to reflect how value enters the product, how it moves, where counterparties sit, what customer types create higher risk, and how that drives control design. A generic risk assessment that could apply to any fintech is not a defensible risk assessment, and experienced reviewers can tell the difference in minutes.

Program maintenance

Controls cannot remain static while the business changes. New corridors, new products, new customer profiles, and new transaction patterns all create reasons to revisit monitoring logic, onboarding controls, escalation rules, screening thresholds, and documentation standards. If your risk assessment was written before your last product launch, it has already drifted from the reality it is supposed to describe.

Governance ownership

AUSTRAC’s compliance guidance points to obligations around governing bodies, senior managers, and AML/CTF compliance officers. The exact organizational structure will vary, but named accountability remains central. Governance ownership means someone is personally accountable for the program and not just listed on an org chart and copied on emails.

Evidence discipline

If a firm changes its controls, it should be able to show what changed, why, who approved it, and how the transition risk was managed. If that evidence sits in scattered inboxes, inconsistent meeting notes, or undocumented team knowledge, the weakness is not administrative. It is governance. The control may be real. The evidence that it is governed is not.

AMLI Analysis: This is where “policy-complete” and “operationally ready” start to separate. One can live in a shared folder. The other has to survive scrutiny.

What better-prepared firms are doing differently

The firms adapting best to this environment are not necessarily the biggest. They are usually the ones treating AML as an operating system rather than a document set. In practice, that looks like a consistent set of habits:

-

They review their risk assessment when product scope changes, not on an annual calendar that disregards the business's actual activities.

-

They involve compliance before launch, not after a partner asks questions.

-

They maintain monitoring logic through a documented change process, so every threshold decision has a rationale and an approval record.

-

They define minimum standards for investigation notes and escalation records, not because an auditor asked, but because inconsistent case handling is a control failure.

-

They keep a remediation log with named owners and due dates, and they close items rather than accumulate them.

-

They know where their evidence is and can produce it the same day someone asks for it.

In other words, they reduce the distance between policy and practice.

Modern AML friction is rarely caused by the absence of a policy document. It is caused by the distance between what the policy says and what operations actually do. That is becoming more important because more often, it comes from mismatch. The policy describes one process. The business runs another. A diligence review, audit, or supervisory interaction exposes the gap.

If you are not confident your program would pass this test, https://amlincubator.com/book-a-call.

What a weak program and a strong program actually look like

The gap between a weak and strong AML program is not usually about intent. Most compliance teams know what good looks like. The gap is almost always about evidence and operational discipline. Here is what that difference looks like in the areas that matter most during a review.

Risk assessment

|

Weak program |

Strong program |

|

Generic template with product categories checked off |

Describes specific product flows, customer segments, and geographic exposures with named risk owners |

|

Last updated at program launch |

Reviewed and updated when product scope changes, with a change log |

|

Risk ratings assigned without documented rationale |

Risk ratings with documented reasoning tied to actual customer and transaction data |

Transaction monitoring

|

Weak program |

Strong program |

|

Default vendor thresholds applied without review |

Thresholds calibrated to actual customer behaviour, with tuning records |

|

Alert volume treated as success metric |

Alert quality and closure consistency tracked as primary metrics |

|

Cases closed without consistent documentation |

Standardised case notes covering trigger, data reviewed, decision, and approval |

Evidence and governance

|

Weak program |

Strong program |

|

Policy documents in a folder, not connected to operations |

Policies reflect current product reality and are reviewed on a defined cycle |

|

Evidence scattered across inboxes and meeting notes |

Centralised evidence pack that can be produced the same day it is requested |

|

No remediation tracking |

Active issues log with named owners, due dates, and documented closure |

AMLI Analysis: Partners and auditors have seen enough programs to know which column they are looking at within the first fifteen minutes of a review. The goal is not to seem organized. It is to actually be organized.

Execution reality: what global fintech teams should be doing now

For firms outside Australia, the practical response to the AML reform of 2026 is to use this reform as a structured stress test on what already exists.

A sensible immediate review covers six areas:

-

Whether the current risk assessment still matches the actual product and customer base.

-

Whether monitoring logic has been reviewed in line with current customer behavior and transaction patterns.

-

Whether governance owners are clearly named and actively accountable and not just listed.

-

Whether change decisions are documented with rationale and approval records.

-

Whether case handling standards are consistent across the team.

-

Whether the firm can produce a coherent evidence pack without reconstructing history.

Most firms that run this review honestly will find two or three areas where the answer is uncertain. That uncertainty is the gap. And the gap is usually not about missing tools or lacking knowledge. It is about the distance between knowing what good looks like and having built the operational discipline to sustain it.

That kind of review is valuable even where no immediate legal change applies. It shows whether the business is building controls that scale with scrutiny rather than only with volume.

AMLI Analysis: This is often the point where founders realise the real bottleneck is not awareness of AML. It is operational discipline.

Frequently asked questions

Q) What is Australia’s AML reform 2026?

Australia’s AML reform 2026 refers to the changes introduced by the Anti-Money Laundering and Counter-Terrorism Financing Amendment Act 2024. Existing reporting entities will face updated obligations from March 31, 2026. From July 1, 2026, around 80,000 new tranche 2 businesses, including real estate agents, lawyers, accountants, and precious metals dealers begin entering the AML CTF Australia regime for the first time.

Q) Does Australia’s AML reform affect companies outside Australia?

Not directly through AUSTRAC’s jurisdiction. However, the reform signals a global supervisory shift toward outcomes-based compliance, a model already being adopted by FCTF, the EU AMLA, the UK FCA, FinCEN in the US, and FINTRAC in Canada. Non-Australian fintechs, MSBs, and VASPs are increasingly judged against the same operational expectations by partners, auditors, and regulators in their own markets.

Q) What is the difference between AML reform and AML compliance?

AML reform refers to changes in regulation: new laws, expanded scope, or updated supervisory expectations. AML compliance is the ongoing operational practice of meeting those obligations through governance, risk assessments, customer due diligence, monitoring, investigations, and evidence. Reform changes the standard. Compliance is how firms meet it.

Q) What should a fintech do now in response to Australia’s 2026 AML reform?

Even if you are not subject to AUSTRAC directly, the reform is a useful prompt to stress-test your own program. Review whether your risk assessment still matches your current product, whether monitoring logic reflects actual customer behavior, whether governance ownership is clearly named, whether change decisions are documented, and whether you can produce a coherent evidence pack on short notice.

Q) What are tranche 2 entities under Australia’s AML/CTF reform?

Tranche 2 entities are the newly regulated businesses entering the AML CTF Australia regime from July 1, 2026. They include real estate agents, lawyers, conveyancers, accountants, trust and company service providers, and dealers in precious metals and stones. These sectors have previously operated outside the AML/CTF regime. Their inclusion brings Australia into alignment with FCTF recommendations, which have long identified these sectors as higher-risk for money laundering.

Q) Who regulates AML compliance in Australia?

AUSTRAC, the Australian Transaction Reports and Analysis Centre, is Australia’s AML/CTF regulator and financial intelligence unit. It administers the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 and its amendments. More information is available directly on the AUSTRAC website.

Related AMLI resources

If this article raised questions about your own program’s scope, structure, or evidence readiness, these AMLI resources cover the relevant areas in more depth:

Ready to find out where your program stands?

Book a Discovery Call to review your AML operating model, identify control gaps, and assess whether your program is built for current supervisory expectations.

→ https://amlincubator.com/book-a-call